【本文为中英文对照版】上半部分为中文原文,下半部分为英文译文。

[Bilingual Edition] The Chinese version is in the upper p. The English translation follows in the lower p.

注:本报告内销量、售价、折扣、门店数量、盈利测算等所有数据均为市场调研推演估算,未经车企官方核实、非官方财报数据;相关盈亏分析仅为行业学术研究参考,严禁用作加盟投资、商业合作、诉讼索赔、企业经营好坏评判、证券投资等各类决策依据,内容不客观反映鸿蒙智行各品牌及合作车企真实经营、财务现状,任何人依据本文数据产生的经济损失,本文作者不承担法律责任。

核心结论摘要

107万 问界累计销量 截止2026年4月 | 28.5万+ M9累计交付 上市21个月,50万级销冠 | ≈理想 鸿蒙智行月销量 2026年4月32,965 vs 33,460 | -86% BBA 35万+月销 峰值16.35万→现2.3万,腰斩再腰斩 |

截止2026年4月,鸿蒙智行累计销售134.2万,其中问界品牌累计销售107万,占鸿蒙智行总销量的79.7%。问界M9用21个月完成了中国品牌豪华汽车史上的里程碑:50万+价格段连续21个月销冠(2024年2月-2025年10月),50万+新能源车市场中 M9 冠军期平均市占率约 55%,峰值月(2024 年 7 月)超过70%。2025 年11月起丢失月度销冠,但仍稳居高端市场前三。这不是个别爆款,而是一个完整生态在高端市场完成系统性胜利的缩影。

摘要:你为什么应该读完这篇报告

这是一份关于华为造车三年的系统性复盘,全文约1.9万字,八章结构,覆盖从战略逻辑到渠道数据、从竞争格局到经销商投资的完整链条。本篇分析报告是基于上险销量数据、网络公开门店数据与价量库(桑之未调研数据)的交叉分析——一次试图用数字说清楚"华为在汽车行业究竟做对了什么,又在哪里埋下了隐患"的研究尝试。

一 这份报告试图回答五个问题

▸ 问界为什么能在40万+市场站稳?——不只是产品力,更是华为三张核心牌的系统协同,以及BBA恰好在最脆弱的时间窗口失守。

▸ 五界体系,是均衡发展还是一拖四?——智界、享界、尚界进入的价格段,华为赋能的边际价值严重递减;三界发布再多新车,在对应赛道的竞争格局没有系统性改变之前,突破空间极为有限。

▸ 渠道到底有多大?数字口径为何混乱?——"约5,960个授权触点"与"约2,640处物理门店"并不矛盾,但指向不同的分析维度;本报告首次完整拆解三类渠道的分工机制与五界品牌的覆盖边界。

▸ BBA的衰退是否无法逆转?——BBA月销从峰值16.3万辆跌至约2.3万辆,折扣率突破23%;但Momenta+合资品牌的反攻组合正在成型,上汽奥迪E7X已于2026年5月上市,这个故事远未结束。

▸ 经销商还应该投资鸿蒙智行渠道吗?——这是本报告最具争议性、也是行业中首次基于城市分层数据公开披露的分析。答案不是"是"或"否",而是"取决于你在哪个城市、哪个品牌、处于哪个阶段"。

二 六组核心数据,帮你快速定位

维度 | 关键数字 | 解读 |

问界累计销量 | 107万辆 | 占鸿蒙智行总销量79.7%;五界体系的绝对支柱 |

五界2026年4月月销 | 32,965辆 | ≈理想汽车;问界23,223辆独占70%,三界合计8,600辆 |

BBA两年月销降幅 | 宝马−36.5%·奔驰−46.1%·奥迪−42.0% | 折扣率全线突破20%;问界BBA替代效应真实存在(注:销量数据为"2024年4月"与"2026年4月",属于同期单月对比) |

渠道规模 | 约5,960个授权触点 / 约2,640处物理门店 | 263个城市,覆盖率约90%;三类渠道功能各异 |

问界一线城市单店月均 | 51.7辆(2026年) | 盈亏临界27~48辆;一二线盈利确定性高 |

三界共享门店单店月均 | 6.7辆(2026年) | 低于共享门店盈亏临界;全线亏损/临界;依赖问界输血 |

数据来源:上险数据 / 公开网络数据 / 乘用车价量统计总表;

三 第八章:行业首次披露的经销商投资数据

本报告第八章是目前公开分析中,首次将鸿蒙智行官网门店数据与城市上险销量数据交叉,计算出五界各城市层级单店月均效能,并对照实际盈亏参数(返利留存2%~2.5%、金融单车5,000元、售后1.5次/年毛利率40%)给出分层盈亏结论。

问界:一线51.7辆✅盈利 / 二线35.5辆✅盈利 / 三线28.3辆⚠️临界 / 四线15.5辆❌亏损 / 五线13.1辆⚠️临界

三界共享门店:各层级单店月均约6.7辆,全面低于盈亏临界,一二线❌深度亏损,三四五线⚠️临界

六种投资情形、六个答案,从"★★★★积极考虑"到"★强烈暂缓",覆盖:一二线扩网、代理尊界、三线新建、四线入场、增加三界授权、以"华为概念"仓促入场。

一个核心判断:2025年是渠道扩张期,大多数经销商都能分到红利。2026年,销量下滑约34%而门店仍在增加,效能分化期已经来临。现在是"精挑细选"而非"跑马圈地"的阶段。

四 不同读者的阅读建议

读者角色 | 重点章节 | 核心收益 |

汽车行业研究者需要 | 全文 | 完整的数据链:战略→产品→渠道→竞争→经销商,三年时间轴 |

汽车经销商投资人 | 第八章(必读)+ 第三章 | 首次量化的城市分层盈亏分析;六种投资情形判断 |

品牌/营销从业者 | 第二章 + 第五章 | 五界各品牌现状与三界困境;华为赋能边际价值递减规律 |

对BBA感兴趣的读者 | 第六章 + 第七章 | 替代效应数据验证;Momenta反攻逻辑;冲击能否持续的结构判断 |

对新能源行业感兴趣的读者 | 第一章 + 第五章 | 华为进入汽车的三代模型;三境体系(启境/奕境/华境)战略延伸 |

本报告所有数据仅供研究参考,不构成任何投资建议。数据来源与免责声明见各章节末尾及正文结语。

第一章 华为进入汽车行业的底层逻辑

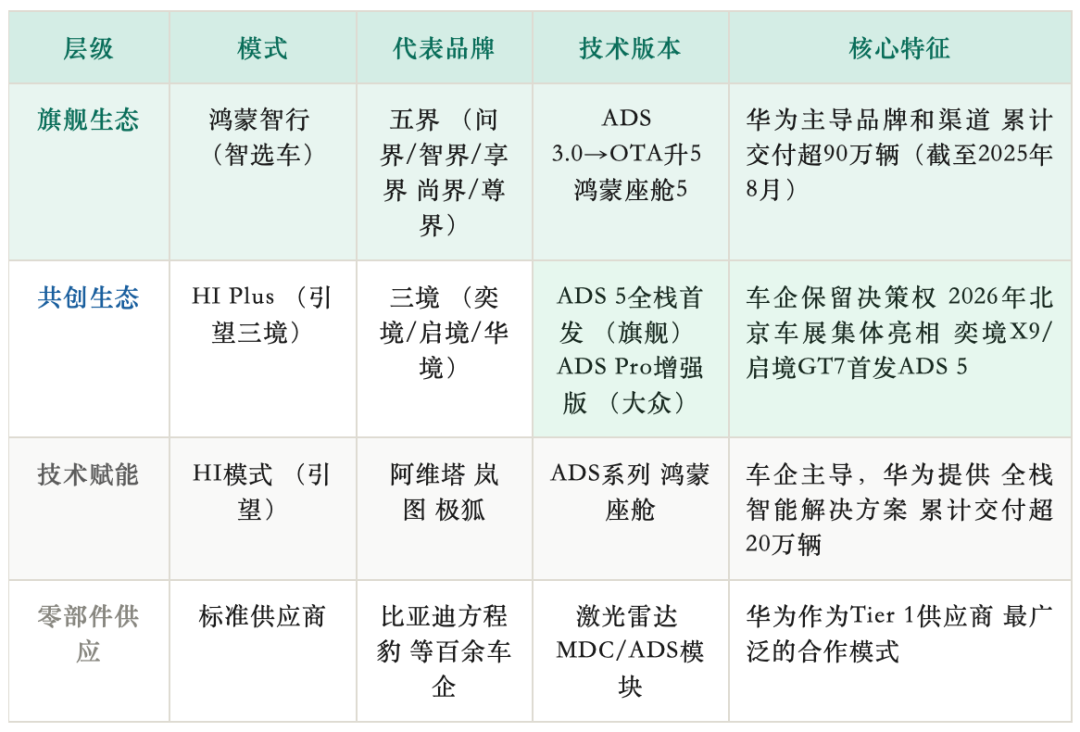

◆ 1.1 合作模式的三次进化

华为并非传统意义上的整车制造商,而是以科技赋能者的身份切入,并随市场验证逐步加深介入深度。华为主导的问界(AITO)品牌是2021年12月发布,鸿蒙智行于2023年9月推出。

2025年截至8月,鸿蒙智行五界体系累计交付超90万辆,HI模式车型累计交付超20万辆。华为已从汽车产业边缘进入舞台中央,与东风、长安、北汽、上汽、广汽等国央企及奇瑞、江淮均建立深度合作。(口径:含批量订单交付,非纯上险数)

◆ 1.2 华为的三张核心牌

传统车企无法复制鸿蒙智行成功的根本原因,在于华为同时掌握三张在汽车行业独一无二的牌:

▸ 智能座舱(鸿蒙HarmonyOS):车载操作系统与手机/家居/办公全生态互联,"手机用户无缝切换"的体验护城河,短期内无竞品能复制

▸ 智能驾驶(乾崑 ADS 4.0→5.0):端到端大模型架构,城区NOA覆盖范围持续扩大,2025 年 ADS 4.0 落地,与小鹏、特斯拉并驾齐驱

▸ 线下渠道(华为授权体验店):全国数千家华为门店直接成为汽车销售触点,购车与换机、购表的消费者画像高度重叠,获客成本远低于传统4S模式

关键判断:华为的优势不在于某一项技术领先,而在于三张牌的协同效应。消费者购买问界,本质上是购买"华为生态成员资格",这种消费决策逻辑是BBA用降价无法对抗的。

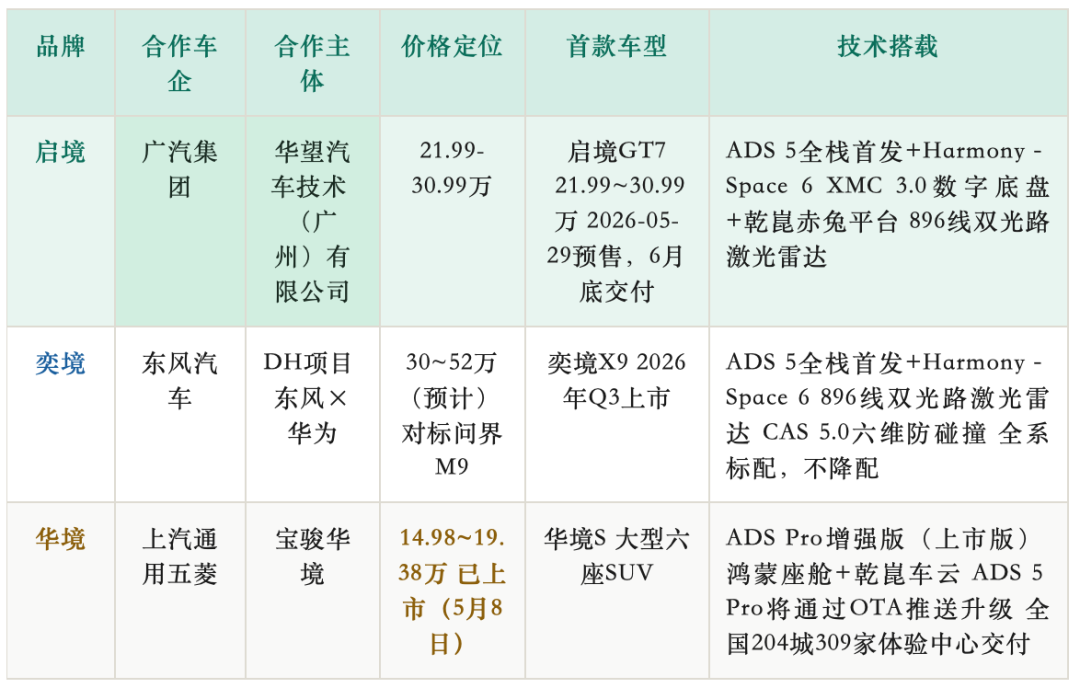

◆ 1.3 三境体系:HI Plus模式的战略延伸(2025~2026年)

五界体系在市场上的成功验证了"华为背书"的价值,但也暴露了智选车模式的内生矛盾——合作车企(赛力斯、奇瑞、北汽等)话语权过低,智界、享界已开始"谋独立"。三境的HI Plus模式是华为对这一矛盾的主动回应:给大型国企(东风、广汽、上汽通用五菱)保留更多决策自主权,换取更广泛的合作版图,同时将最新一代技术(ADS 5+HarmonySpace 6)优先赋能给三境首发车型。

三境品牌矩阵总览(截至2026年5月)

技术代际:ADS 5发布节点与搭载路径

2026年4月23日,华为乾崑两周年技术大会在北京正式发布ADS 5(WEWA 2.0架构)和鸿蒙座舱HarmonySpace 6。此次升级跳过了4.2/4.3等中间版本,属于架构级迭代,核心变化如下:

▸ WEWA 2.0架构:云端世界模型首次引入"多智能体博弈"机制,训练强度较上一代提升10倍,实现"边生成、边学习、边验证"的在线强化学习闭环

▸ 乾崑OS:首发面向自动驾驶专用的操作系统,具备确定性调度引擎和全链路安全模型,紧急场景中车内信号时延降低30%

▸ 安全指标:基于累计100亿公里辅助驾驶里程数据优化,安全性达人类司机的3.69倍;全维防碰撞CAS 5.0覆盖六维方向

▸ 技术普惠:ADS Pro同步更新,将城市NCA使用门槛下沉至15万级,城区NCA使用占比从22%提升至29%

五界 vs 三境:两种模式的本质差异

三境的战略意义:华为的双轨扩张逻辑

扩大朋友圈:五界体系证明了"华为背书"的商业价值,但也因华为话语权过强导致合作车企心存顾虑。HI Plus模式给大型国企(东风、广汽、上汽通用五菱)保留更多自主权,使华为的合作版图扩展至六大国央企全部覆盖,"朋友圈"更大、更稳。

技术首发权给三境:三境旗舰车型(奕境X9、启境GT7)成为ADS 5的全球首发量产阵营,比五界现有在售车型领先一个技术代际(五界将通过OTA追平)。这既是对三境合作车企的激励,也是华为向市场展示"最新技术就在这里"的信号弹。

价格下沉打开新市场:华境S以14.98万元起售,是鸿蒙智行/引望生态中首次大规模进入15万价格带的产品,将华为乾崑智驾的使用人群从30万+高端消费者扩展到大众市场,与五界的高端定位形成互补而非竞争。

奕境X9:央企首个全栈原生共创标杆

奕境X9是东风汽车作为汽车央企与华为乾崑深度共创的首款旗舰产品,定位30~40万级家庭旗舰大六座SUV,直接对标问界M9和理想L9。预计售价38~52万,2026年第三季度正式上市。

▸ 硬件领先:全系标配896线双光路图像级激光雷达,对低矮障碍物识别距离162米,雨雾天感知精度提升40%,硬件规格超越当前五界主力车型

▸ 安全强化:首创2400MPa超高强度钢车身(行业主流的1.2倍强度)+三层防弹级电池装甲,安全叙事是核心差异化卖点

▸ 尺寸旗舰:车长5301mm,轴距3120mm,欧洲团队参与底盘调校,全铝底盘结构

▸ 渠道目标:全年服务触点达300个,采用"1+N"用户中心+商超店模式

关键问题:奕境X9能否复制问界M9的成功?两车的核心差异在于:M9背靠赛力斯多年问界品牌积累和华为渠道资源,奕境X9是全新品牌从零开始,品牌认知建立需要时间和持续投入。但奕境X9在硬件配置(896线雷达)和技术版本(ADS 5首发)上确实比M9当前版本有代际优势,价格也可能更具竞争力(预计38万起 vs M9的47万起)。

华为汽车生态版图:截至2026年5月全景

截至2026年5月,华为已与东风、长安、北汽、上汽、广汽等国央企及奇瑞、江淮等建立不同深度的合作,在售或即将上市的华为系车型覆盖15万至100万+全价格带,智驾ADS累计整车搭载量突破170万辆,辅助驾驶累计里程超100亿公里。

第二章 鸿蒙智行五界体系:从单点突破到全价位覆盖

◆ 2.1 五界品牌矩阵

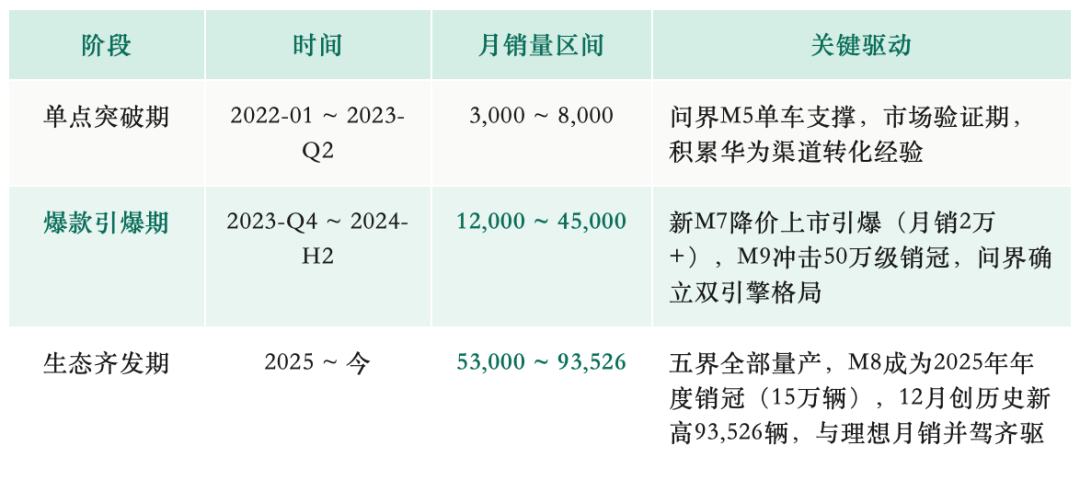

◆ 2.2 销量演变:三个阶段

鸿蒙智行的销量成长可分为三个阶段,每个阶段均由关键车型驱动:

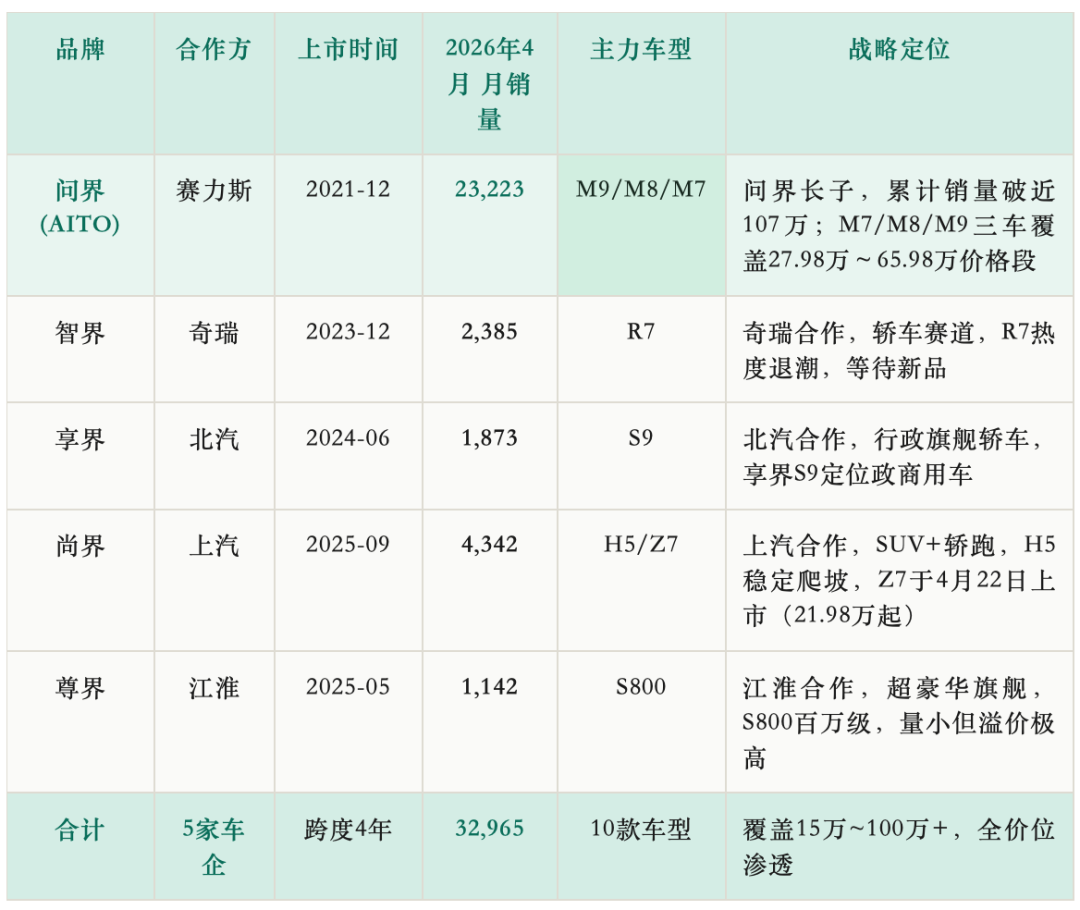

2025年12月鸿蒙智行月销93,526辆,接近理想同期的两倍水平。问界M8单车年销超15万辆,成为2025年30~40万价格段新势力年度销冠,延续了新M7在2024年的同类纪录。

◆ 2.3 各品牌现状与隐忧

问界(AITO):体系支柱,换代切换期需关注

▸ M9:50万+月销已从峰值1.8万(2024-07)回落至约3,000~5,000水平(2026年初),2025年Q4仍维持在7,500~9,200水平,2025款上市后逐步回暖。21个月50万+价格段连续21个月销冠(2024年2月至2025年10月),该纪录已于2025年11月被蔚来ES8终结,2025年11月起连续多月位居前三。

▸ M8:2025年销量冠军,年销超15万辆,订单量曾突破9万,填补了M7和M9之间的价格空白(35~46万)

▸ M7:2024年新势力年度销冠,换代期间销量有所波动,M6接棒爬坡中

智界:热度退潮,等待新品刷新

▸ R7曾是奇瑞联合华为的首款轿跑型SUV,上市初期市场反响尚可,但2026年月销已降至1,910辆左右,品牌声量明显弱于问界

▸ 折扣率从6%升至9.5%,显示产品竞争压力;奇瑞与华为宣布"智界2.0战略",成立独立法人,预计新品发布后有望重新激活

享界:高折扣率与销量波动并存

▸ S9定位行政旗舰轿车,月销1,873辆,销量波动大,难以形成稳定爬坡

▸ 北汽与华为深化合作,正在构建享界专属渠道,当前渠道建设滞后是主要制约

尚界:折扣率攀升,Z7潜力待观察

▸ H5月销稳定在3,852辆,但折扣率持续攀升:4.89%(2025-10)→11%(2026-04),是五界中折扣恶化最快的品牌,需重点关注

▸ Z7刚于2026-04上市(首月490辆),作为轿跑车,上市曲线需更长时间验证

尊界:超豪华小众,价格体系最稳健

▸ S800定价78.98~102.8 万级,折扣率始终维持4.5~5.6%,是五界中价格体系最健康的品牌

▸ 月销量约1,000辆级别,典型的小众超豪华产品,一线城市贡献占比接近39%,与其消费者画像(高净值人群)高度吻合

第三章 渠道网络:华为的第三张核心牌

数据来源:网上公开信息 | 月销数据:上险登记口径(2026年4月)

◆ 3.1 五界网络规模(2026年6月快照)

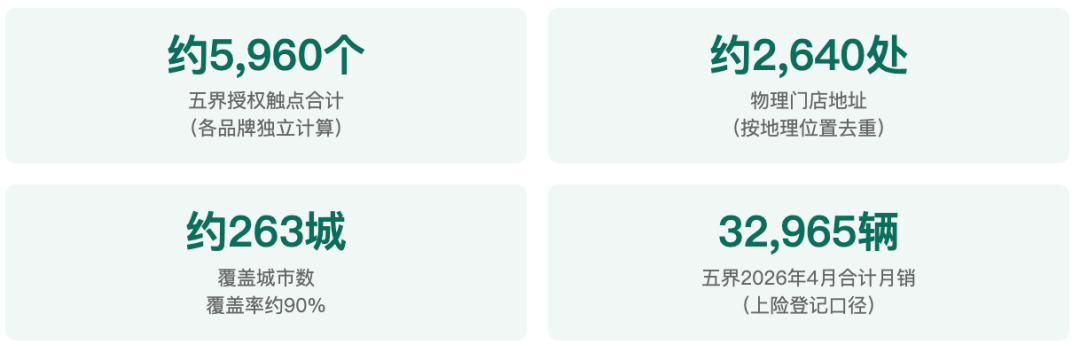

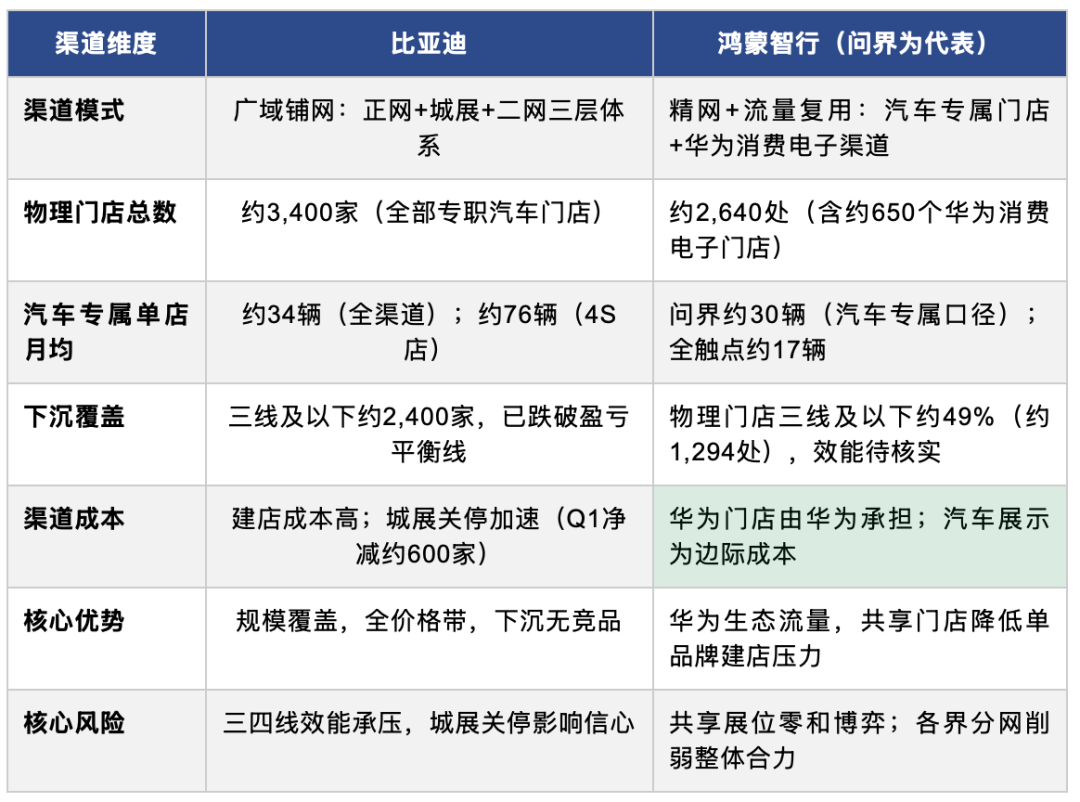

截至2026年6月,鸿蒙智行五界授权触点合计约5,960个(五界各自独立计算);按地理位置去重后,实际物理门店约2,640处,覆盖约263个城市,全国城市覆盖率约90%。

注:授权触点含共享门店(同一物理门店被多品牌授权时重复计入);物理门店按地理位置去重。数字均为近似值,以上为网络公开数据,真实数据以车企发布数据为准。

数据口径说明:授权触点 vs 物理门店

五界共有约1,320个鸿蒙智行用户中心同时获得多个品牌的销售授权,因此:五界授权触点合计约5,960个 > 物理门店约2,640处。两个数字服务于不同分析目的——前者衡量各品牌的渠道广度,后者用于与竞品门店数横向比较。

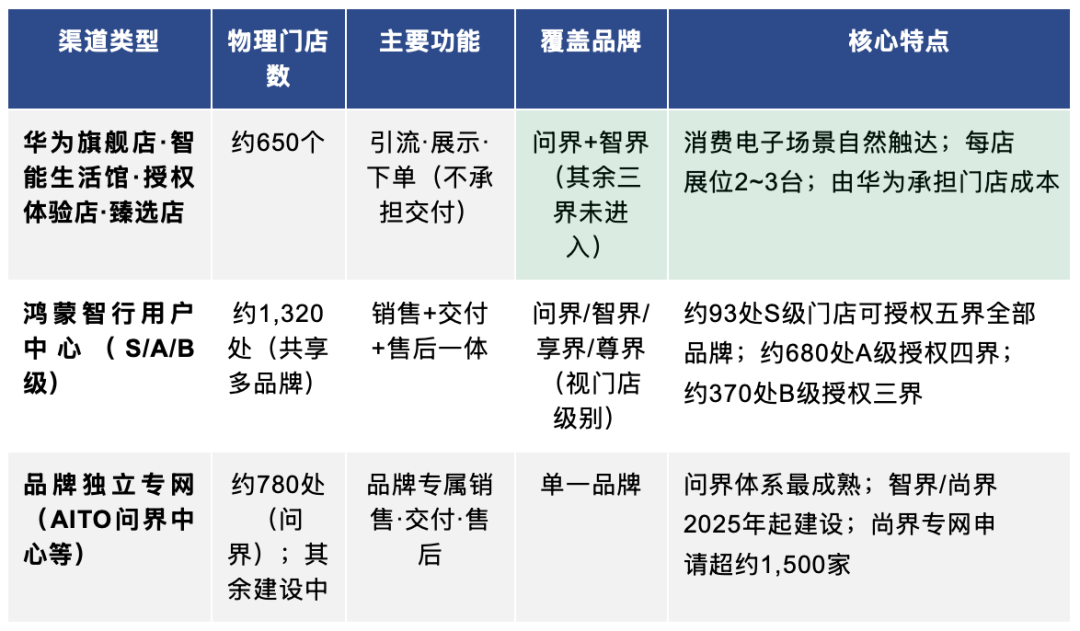

◆ 3.2 三类渠道的分工机制

鸿蒙智行渠道体系由三类门店构成,各类门店在功能和品牌覆盖上存在明确分工。理解这套分工机制,是理解华为渠道护城河的关键。

注:尚界独立用户中心正在加速建设,部分已归入鸿蒙智行用户中心共网运营

① 华为消费电子渠道——问界独有的流量入口

约650个华为旗舰店(11家)、智能生活馆(约457家)、授权体验店(约175家)和臻选店(3家)中,问界、智界全系获得展示授权;享界、尊界仅核心高端门店专属展示;尚界暂未进入华为商超渠道,独立专网建设中。这一渠道的价值不在于成交量,而在于流量质量——消费者在购买华为手机或平板时,无意间完成了对汽车的首次感知,获客成本远低于传统汽车展厅。

▸ 问界约570个华为渠道触点(占问界总触点42%),是问界最核心的差异化竞争优势,其他四界无法复制

▸ 智界约630个华为渠道触点(占45%),覆盖广度接近问界,但问界历史积累更深、陈列更优先

▸ 享界、尊界、尚界华为商超渠道占比极低或为零,完全依赖鸿蒙智行专属汽车门店

② 鸿蒙智行用户中心——按门店级别决定卖几个品牌

鸿蒙智行用户中心是五界共享的汽车专属销售与交付网络。数据显示,约1,320个物理门店同时获得2个以上品牌授权:约93个S级旗舰用户中心(面积约8,000㎡+)可销售五界全部品牌,约680个A级用户中心授权四界,约370个B级门店授权三界,约180个城市展厅仅授权两界。同一门店展位资源是零和博弈——展位和销售团队精力向问界高度集中,是智界/享界/尊界/尚界单店效能低于问界的核心渠道原因。

③ 品牌独立专网——分网化趋势正在加速

问界是最早建立品牌独立专网的品牌(约780个AITO问界用户中心),与鸿蒙智行共网并行运营。2025年起,智界和尚界相继宣布建设独立渠道,享界也在筹划。这一趋势揭示了智选车模式的内生矛盾:合作车企在依托鸿蒙智行渠道获得销量的同时,也在追求更强的品牌独立性和渠道话语权。

▸ 尚界专网申请经销商已突破约1,500家,专网规模潜力远超现有官网触点数量

▸ 独立分网对各品牌销量增长有帮助,但削弱了鸿蒙智行整体生态的渠道合力

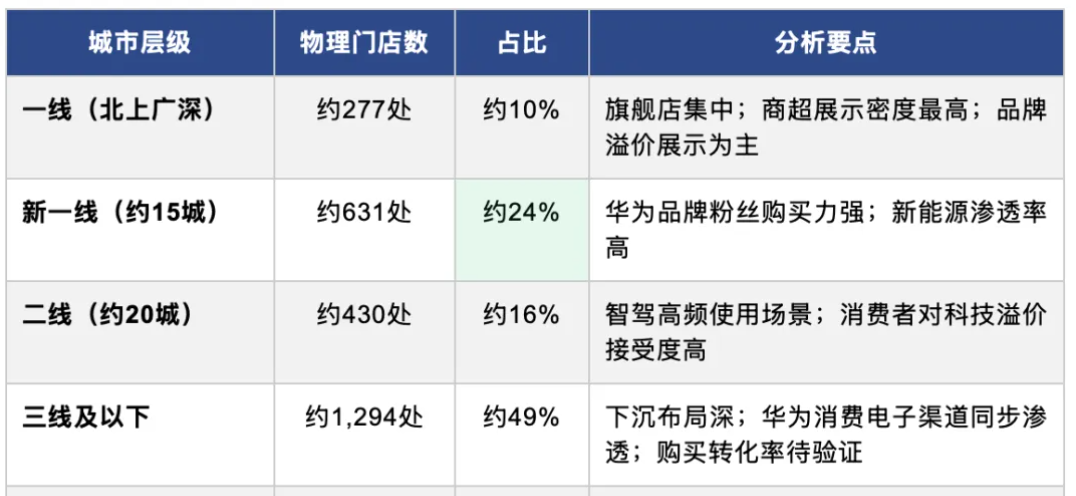

◆ 3.3 地理覆盖:华东华南领跑,三四线接近半数

从物理门店(约2,640处)的地理分布看,五界渠道呈现出「华东华南重镇化+三四线广覆盖」的双重特征。广东、浙江、江苏为前三省,合计约占物理门店总数的28%。与此同时,三线及以下城市门店约占49%,华为消费电子渠道将品牌触达延伸至全国绝大多数城市。

◆ 3.4 渠道效率:不同口径下的单店效能

单店效能分析须区分「华为引流触点」和「汽车专属门店」——两者功能完全不同,不能用同一分母计算。汽车专属门店(用户中心+体验中心+交付中心)是合理的效能基准:

*单店月均=品牌月销÷汽车专属门店数(用户中心+体验中心+交付中心),华为直属渠道不纳入分母

参考:比亚迪全渠道约34辆/月/店;比亚迪4S店口径约76辆/月/店(2026年1-4月)

◆ 3.5 与比亚迪渠道模式的结构性对比

鸿蒙智行与比亚迪代表了中国新能源渠道的两种典型范式。比亚迪以约3,400家专职汽车经销商构成广域覆盖网络;鸿蒙智行以约2,640个物理门店(含约650个华为消费电子渠道)构成精网+生态流量复合模式。

◆ 3.6 渠道内生矛盾:分网化与合力的博弈

约1,320个多品牌共享门店中,同时持有五界全部授权的约93个,持有四界授权的约680个,持有三界授权的约370个——授权品牌越多,单一品牌获得的实际展示资源越稀薄,这是渠道内生矛盾的数据体现。

▸ 智界、尚界已宣布建设独立渠道;享界筹划独立建网;问界早已拥有独立的AITO用户中心体系

▸ 分网后各品牌依据自身定位制定差异化建店标准,降低经销商压力,但华为生态整体合力被稀释

▸ 问界约780个AITO专属用户中心品牌独立性最强;其余四界仍高度依赖共享网络

渠道分网化折射出智选车模式的内生矛盾:合作车企借助鸿蒙智行品牌背书获得销量的同时,也在追求渠道独立性。华为的挑战在于如何在各界加速分网的过程中,维持「鸿蒙智行」整体品牌的渠道向心力,避免生态碎片化。

数据说明:渠道数据来自公开信息。月销来源:上险数据(2026年4月)。仅供研究参考。

第四章 产品力解析:问界为何能站稳40万+市场

◆ 4.1 核心竞品配置横向对比

注:配置数据来自汽车配置数据库,仅供参考,请以厂商官方数据为准。

◆ 4.2 问界产品力的四大支柱

① 增程技术路线:精准契合中国用户需求

▸ 问界M9增程版占销量约85~92%,成交均价约48万,纯电版仅占8~15%,说明用户主动选择增程而非被动接受

▸ 增程解决了中国高端用户的核心痛点:长途无续航焦虑,日常纯电出行,无需在充电便利性上妥协

▸ 折扣率仅5~7%,相比同价位BBA(折扣率20~30%)具有显著价格体系优势,保值率连续9个月大型SUV第一

② 华为全栈智驾(ADS 3.0---ADS5.0):体验代差

▸ 端到端大模型架构,无需高精地图,城区NOA持续OTA迭代,用户实际体验领先于大部分竞品

▸ 2025年问界M9 NPS高达85.2,连续多期位居车型总榜首位,智驾体验是用户最主要的推荐理由之一

▸ BBA高端车型的ADAS系统与华为ADS 3.0存在明显代差,且BBA电动化转型滞后,无法在短期内弥合

③ 鸿蒙座舱:生态黏性构建超级壁垒

▸ 华为手机用户(数亿规模)直接转化为潜在车主,车机互联的使用体验形成强绑定

▸ 鸿蒙OS车载系统支持多屏联动、远程控车、与华为穿戴设备联动,竞品无法复制这一生态协同

④ 华为门店渠道:低成本获客,高端品牌背书

▸ 华为授权体验店承担汽车展示和首次接触功能,购车决策与数码消费场景自然融合

▸ 华为品牌在消费者心中的科技溢价,直接转移到问界车型上,用户愿意为"华为的车"支付40~50万

第五章 竞争格局:华为赋能的边际价值与三界困境

以上数据揭示了一个核心结构性问题:鸿蒙智行五界的成败,本质上取决于华为技术和品牌赋能在各价格段能发挥多大的差异化价值。数据表明,这一价值随价格下行而快速递减——35万以上,"华为的车"是真实的溢价理由;20万以下,这个标签的吸引力已经相当有限。

◆ 5.1 问界与尊界:战略成立,护城河真实

问界的核心竞争逻辑是在BBA智能化转型滞后期间完成截流。2021~2026年,BBA(35万+市场) 三家月销合计已从约16.35万辆腰斩至约2.3万辆,折扣率全线突破20%以上(奥迪27.5%、宝马23.3%、奔驰19.5%),价格体系崩溃,大量客群流向新势力品牌。

但这个窗口不是永久的。BBA在智能化上的落后是时间债务,不是能力缺陷——奔驰、宝马均已与多家中国智驾公司展开深度合作,预计2026~2027年将推出具备L2+智驾能力的车型。问界当前优势的本质是BBA智能化转型期间的截流红利,窗口期估计还有2~3年。这也正是问界在该窗口期快速扩渠道、提升品牌心智的战略用意所在。

尊界定位自洽。月销1,142辆、均价78.1万、折扣率5.7%——超豪华品牌不追求规模,追求在百万级市场建立华为的品牌锚点。这个定位与问界的逻辑一致:在BBA豪华品牌大幅折价的市场空隙中,用技术溢价填补空缺,执行逻辑清晰。

◆ 5.2 三界困境:选错了战场还是战略过于乐观?

智界、享界、尚界进入的价格区间,竞争者众多且各具比较优势,而华为的技术赋能在这些价格段无法成为决定性的购买理由。发布更多车型能解决"有没有得买"的问题,但解决不了"为什么要买你"的问题。

① 智界:陷入最拥挤的赛道,且缺乏差异化

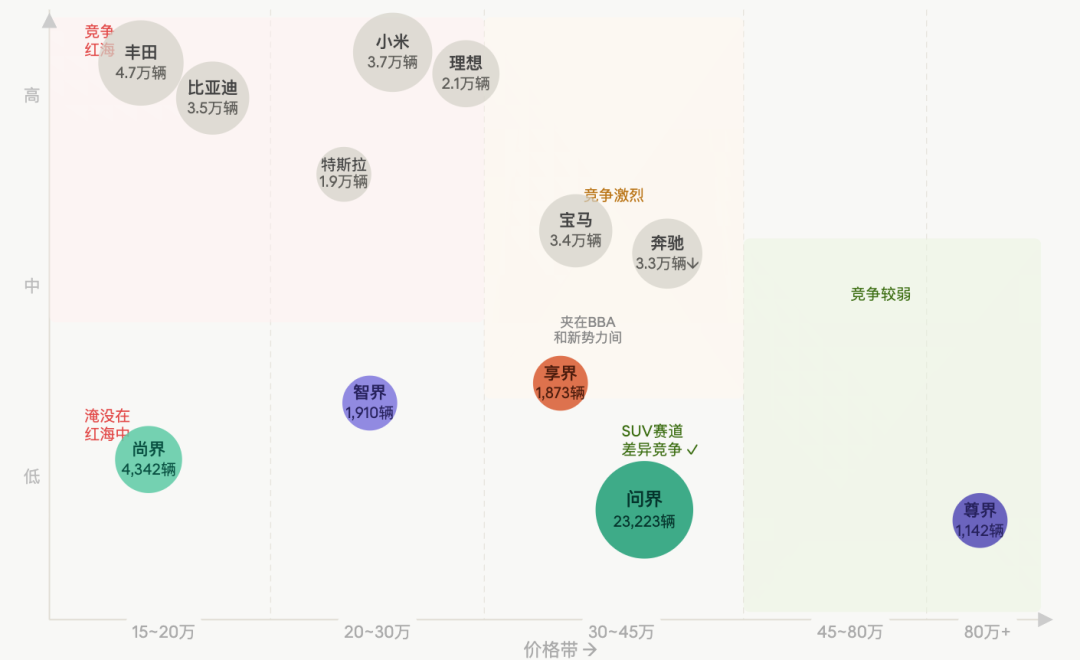

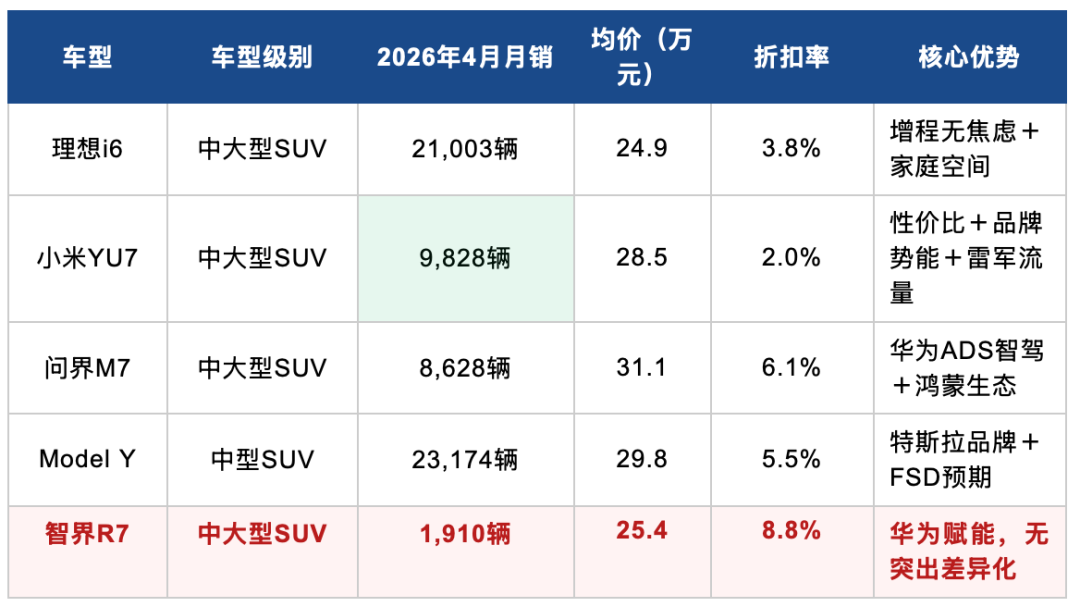

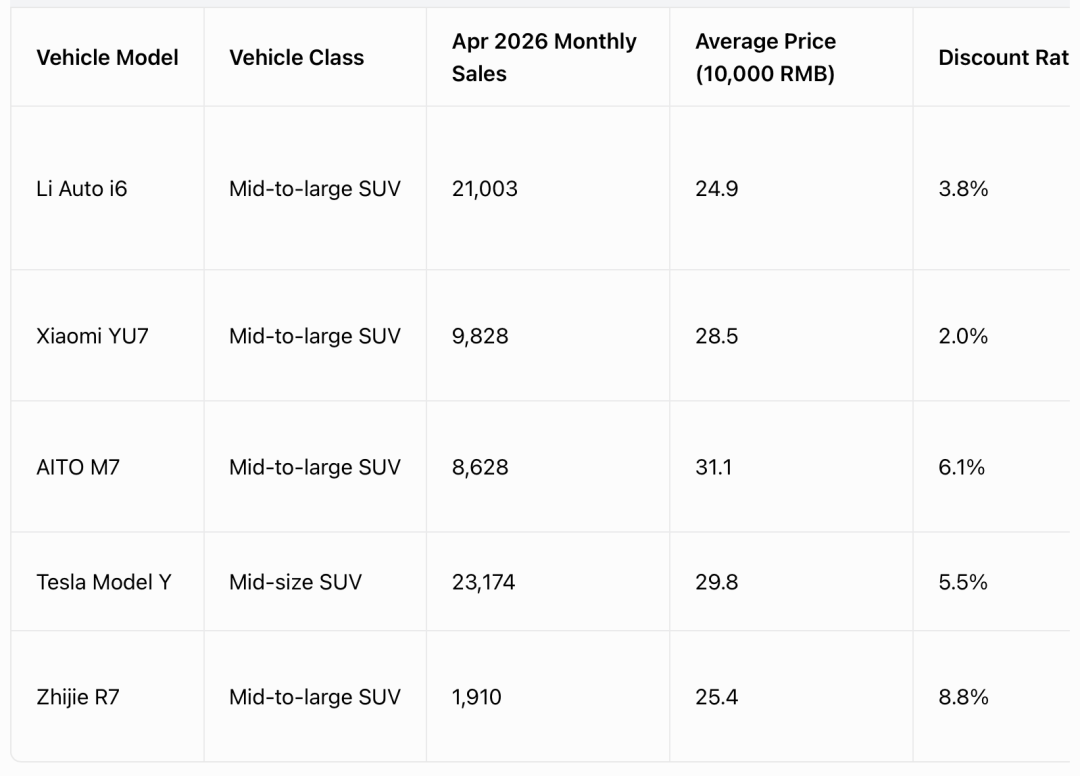

2026年4月,智界R7月销1,910辆,而同赛道SUV中,理想i6月销21,003辆(差距11倍)、小米YU7月销9,828辆(差距5倍)、问界M7月销8,628辆(差距4.5倍)。在20~30万中大型SUV赛道,智界R7同样处于竞争劣势。

数据来源:乘用车价量统计总表,2026年4月上险口径

SUV赛道主流折扣2~6%(理想3.8%、小米YU7 2.0%、问界M7 6.1%),智界R7折扣率8.8%,高于赛道均值,竞争压力真实存在。

8.8%的折扣率是最直接的信号——在同赛道SUV竞品普遍维持2~6%折扣的情况下,智界只能靠价格维持出货量,说明产品本身没有实现对竞品的溢价。奇瑞拥有优质的工程能力,但品牌力不足以支撑华为技术加持后的价格预期。智界需要的不是新车型,而是一款能够在SUV赛道打造出「非它不可」口碑的爆款。

② 享界:定位最尴尬,购买逻辑尚待重构

享界S9定价32~40万,瞄准行政轿车市场。这一价格带面临双重挤压:上方是折价销售的BBA(奔驰C级仍有品牌溢价);下方是小米SU7 Pro(28.5万)等高性价比新势力。更根本的困难是,行政轿车的核心购买逻辑是"商务场合的社交信号",而这一逻辑在新能源时代尚未完成重构——在商务接待场景,消费者仍普遍认为奔驰或宝马的品牌信号强于享界。这是时间和认知问题,不是产品问题,增加车型无法加速这一过程。

③ 尚界:进入了一个华为品牌几乎帮不到的战场

尚界H5对应15~20万SUV赛道,竞争者的月销体量令人咋舌:

竞争品牌 | 2026年4月月销(万辆) | 核心优势 | 华为赋能能否对抗 |

合资(日美德系) | 5.5万辆 | 可靠性口碑+保值率+合资品牌信任 | 几乎不能 |

比亚迪(含方程豹) | 2.5万辆 | 垂直整合成本优势+新能源先发积累 | 基本不能 |

尚界H5(估算) | 约3,900辆 | 华为鸿蒙座舱+智驾 | 差距悬殊 |

在15~20万价格段,消费者的核心购买考量是可靠性、保值率和性价比,而非智驾体验或鸿蒙座舱流畅度。这个价格段的用户群体与问界的核心客群(追求高端智能体验的中高收入群体)存在明显差异,华为的品牌溢价在此几乎无法兑现。上汽虽有强大的渠道动员能力(专网申请超1,500家),但用渠道规模弥补产品差异化不足,只会加速关店。

◆ 5.3 一个简洁的结构性结论

品牌 | 赛道选择 | 华为赋能有效性 | 战略评估 |

问界 | 高端SUV(30~55万) | 高——恰好是BBA换购目标客群 | ✅ 逻辑清晰,执行到位 |

尊界 | 超豪华(80万+) | 高——百万客群看中技术溢价 | ✅ 精网蓝海,量小质精 |

智界 | 20~30万中大型SUV | 中低——该价段不缺智能技术品牌 | ⚠️ 战场选择值得商榷 |

享界 | 行政轿车(32~40万) | 中——商务购车逻辑未重构 | ⚠️ 被动等待认知转变 |

尚界 | 15~20万SUV | 低——该价段购买逻辑与华为赋能错位 | ❌ 进入了错误的战场 |

鸿蒙智行五界的本质是"两强三弱"格局,而非五界均衡发展。问界和尊界的成功有清晰的竞争逻辑支撑;智界、享界、尚界面临的不是执行问题,而是赛道问题——在各自价格段,华为的差异化价值尚不足以构成购买决策的主导因素。三界发布再多新车,在对应赛道的竞争格局没有出现系统性变化之前,整体体量的突破空间有限。

第六章 对豪华品牌的冲击:数据证明替代效应真实存在

◆ 6.1 40万+市场的权力转移

2024年2月,AITO品牌首次出现在40万以上市场,当月成交均价约50.9万元。两个月后,问界跃居该市场第三位(仅次于奔驰、宝马),月销量超过1.3万辆,而同期奥迪在该价位段已跌至3,000~5,000辆。

BBA高端价位折扣率恶化:以价换量仍难止血

品牌 | 2023年初折扣率 | 2026年折扣率 | 恶化幅度 | 35万+月销变化 |

宝马 | 14.4% | 23.5~28.8% | +14pp | -91.1% |

奔驰 | 7.9% | 19.3~21.7% | +12pp | -80% |

奥迪 | 18.1% | 27.2~29.0% | +11pp | -96.2% |

保时捷 | 3.8% | 11.3~15.7% | +10pp | 缓慢下滑 |

雷克萨斯 | 7.4% | 17.6~19.7% | +14pp | 缓慢下滑 |

数据说明:奥迪35万+月销从峰值4.4万辆跌至不足1,600辆,即便折扣率从14%扩大至25%仍未止住,说明降价已无法弥合产品力代差。(注:以上展示为典型低值区间;实际月销波动较大,宝马/奔驰高峰月可达2~4万辆。数据来源于价格监测数据库,请以厂商官方及权威机构披露为准)

◆ 6.2 替代关系的三个维度

① 直接销量替代

▸ 国产高端品牌在30万以上市场的份额在2025年上半年已突破35%,五年前不足10%;50万以上市场份额更突破60%

▸ 部分奔驰/宝马/奥迪经销商已开始转向代理中国新能源品牌,渠道资源正在迁移

② 消费者心智替代

▸ 问界M9用户中,来自BBA换购的比例显著,高净值群体将问界M9视为"新豪华身份标签"

▸ 问界M9连续9个月大型SUV保值率第一,打破了"国产车保值率低"的固有认知,这是品牌向上最难的一关

▸ NPS连续多期第一意味着现有车主的强推荐行为,口碑已形成自发传播飞轮

③ 技术溢价重构

▸ 传统豪华品牌的溢价来自发动机调校、底盘工程、品牌历史,这些在智能电动时代的权重正在降低

▸ 华为ADS智驾、鸿蒙座舱、OTA持续进化,代表了新时代的"科技溢价",且是消费者每天都能感知到的体验

▸ BBA的新能源车型(宝马iX、奔驰EQS等)折扣率同样大幅扩大,说明品牌溢价无法有效转移到电动平台

第七章 冲击能否持续?结构性判断

◆ 7.1 支撑持续冲击的三个结构性力量

力量一:技术护城河仍在加深。 华为ADS每季度OTA迭代,智驾能力持续领先。BBA在智驾层面选择与Momenta合作而非自研——宝马新世代iX3搭载Momenta方案(计划年底上市),上汽奥迪E7X已于粤港澳大湾区车展正式上市(26.98万起),首发Momenta R7强化学习世界模型,奔驰亦在推进合作。Momenta城市NOA在第三方供应商中占比约60%,是华为乾崑在智驾领域最具竞争力的挑战者。然而截至2026年5月,华为ADS已进入5.0时代(WEWA 2.0架构),搭载量突破170万辆、辅助驾驶里程超100亿公里,数据飞轮优势短期内难以撼动。智驾赛道已从"有无"之争进入"谁更好"的深度竞争阶段。

力量二:价格体系相对健康,折扣率未失控。 问界M9折扣率维持在5~7%,相比BBA的20~30%折扣,保留了充足的品牌溢价空间。尚界折扣率上升(11%)需关注,但旗舰车型M9的健康折扣是体系稳定器。

力量三:产品矩阵不断完善,价格带持续下探。 尚界H5(15.98万起)是鸿蒙智行首次进入20万以下市场,五界体系从约16万到100万全覆盖,渗透能力大幅提升。越来越多的价格带消费者被"含华量"触达。

◆ 7.2 需要警惕的三个风险

风险一:各品牌内耗——渠道资源争夺

五界10款车型集中在华为门店或鸿蒙智行中心展示,超出了单一门店的承载能力,渠道资源争夺加剧。智界、享界已开始独立建渠道("X界2.0战略"),这既是成长的必要一步,也意味着华为对各品牌的直接管控力在降低,品牌差异化面临压力。

风险二:合作车企的话语权博弈

随着智选车模式成熟,赛力斯、奇瑞等合作车企在技术积累和品牌认知上日益依赖华为。一旦合作关系出现变化,各品牌独立运营能力存疑。同时,车企自身技术积累被边缘化的风险长期存在。

风险三:BBA的反攻并非不可能

▸ 宝马新世代iX3搭载Momenta智驾方案,计划2026年底前在华上市,均价约30~40万,直接对标问界M7/M8价格段;上汽奥迪E7X已于2026年5月29日粤港澳大湾区车展正式上市,售价26.98~35.98万元,较预售价下调2万,以更积极定价切入30万级市场

▸ 奔驰MB.OS架构推进电动化转型;合资阵营借助Momenta等国产智驾方案加速本土化,奥迪E7X的"德系驾控+中国智驾"组合是合资品牌反击路径的新样本

▸ BBA仍在中国市场保持数十万辆年销规模,品牌历史、工程底蕴和全球化背书在部分消费者中依然有效

风险四:Momenta联合合资品牌——最具实质性的智驾挑战

BBA在智驾领域选择与Momenta深度合作,而非自研。Momenta已成为国内第三方智驾供应商的绝对龙头,并正借助合资品牌全面渗透30万+高端市场,是华为乾崑在智驾赛道面临的最直接竞争对手。

Momenta的合作阵营(截至2026年5月)

▸ 豪华品牌:宝马(新世代iX3,计划2026年底上市)、上汽奥迪(E7X,已于2026年5月29日粤港澳大湾区车展正式上市,26.98万起)、奔驰(推进合作中)

▸ 合资品牌:丰田、本田、通用(别克至境L7首发R6)、上大众、福特等全球主要车企集团

▸ 规模:北京车展期间超20个品牌、60余款车型搭载Momenta方案;累计定点车型超170款,已交付近70款,搭载量突破70万台(含城市NOA);城市NOA第三方供应商占比约60%

奥迪E7X:合资反击的最新样本

上汽奥迪E7X于2026年5月开启预售,价格28.98~37.98万元,是理解合资品牌反击逻辑的关键样本。其产品策略可以用"三个首发"概括:AUDI新品牌首款SUV、奥迪首款规划L3自动驾驶量产车、Momenta R7首发量产车型。核心配置包括:

▸ 智驾:Momenta R7强化学习世界模型,28个感知硬件(含激光雷达),英伟达Orin X芯片(254TOPS),官方定位"L3级自动驾驶技术"

▸ 三电:宁德时代109度电池(行业首发),CLTC续航751km,900V高压快充(10分钟补能429km),quattro全时四驱,3.9秒零百

▸ 座舱:高通骁龙8295P,59英寸中控屏,Momenta+豆包双大模型,后排21.4英寸星空屏;定价策略极为激进:5月8日以28.98万元预售,5月29日粤港澳大湾区车展正式上市,售价进一步下调至26.98万元起,直接切入理想i8/蔚来ES6竞争区间,较问界M8(35.98万起)低9万元

Momenta vs 华为乾崑:能否对抗?

Momenta的优势:开放生态,可同时赋能20+品牌,数据积累来源更广;R7强化学习世界模型在架构层面与华为ADS 5处于同一技术代际;成本结构更具弹性,有望将高阶智驾下沉至更低价格段;全球化布局(英国/挪威/澳大利亚等10国落地)领先华为系车型。

Momenta的短板:纯粹的智驾算法供应商,不掌握座舱OS(鸿蒙)、车云、车控、车载光等全栈能力;无法提供"车-手-家"生态联动;合作车企各自为政,难以形成华为乾崑那样统一的用户体验标准和OTA迭代节奏;缺乏华为品牌的消费者信任背书。

判断:Momenta+合资品牌的组合,能在智驾单一维度上与华为乾崑形成实质竞争,但无法复制华为"全栈生态"的整体体验优势。真正的竞争胜负,将取决于消费者在购车决策中更看重"智驾算法能力"还是"车-机-家全生态联动"——目前来看后者在30万+高端市场的权重更高,但随着Momenta方案成本持续下沉,这一差距在20万级市场将显著收窄。

◆ 7.3 综合判断:冲击将持续,但进入竞争深水区

短期(2026~2027):鸿蒙智行在40万+市场的主导地位基本确立,M9保持50万+销冠概率极高,BBA反攻力度有限。

中期(2027~2029):随着BBA新世代产品上市,高端市场将进入更激烈的技术竞争阶段,华为需持续保持ADS和鸿蒙座舱的代际领先。问界M9的保值率优势能否持续,将成为品牌溢价的关键验证指标。

长期(2029+):格局取决于华为智驾生态的全球化能力,以及中国高端品牌能否在海外市场复制国内成功。若问界出海路径打通,对传统豪华品牌的冲击将从中国市场蔓延至全球。

第八章 经销商投资决策:数字背后的真实图景

本章基于网络公开数据与城市上险数据(2025年全年、2026年1-4月)的交叉分析,对五界渠道网络的单店效能与经营健康度进行系统梳理,给出面向汽车经销商投资人的结构性判断,而非笼统建议。

◆ 8.1 行业大背景:新能源经销商分化加剧

2025年全行业汽车经销商亏损比例已升至约55.7%,传统燃油车4S店是重灾区。相比之下,新能源品牌经销商盈利比例约43%,远优于行业整体(23.5%)。但"新能源经销商"内部同样高度分化——盈利集中在高端品牌、高单价车型、头部门店,尾部门店与燃油车4S的困境无异。(注:鸿蒙智行分汽车专属门店自行获客、交付和手机店获客,由汽车专属门店交付两种方式,并有对应的返利奖励)

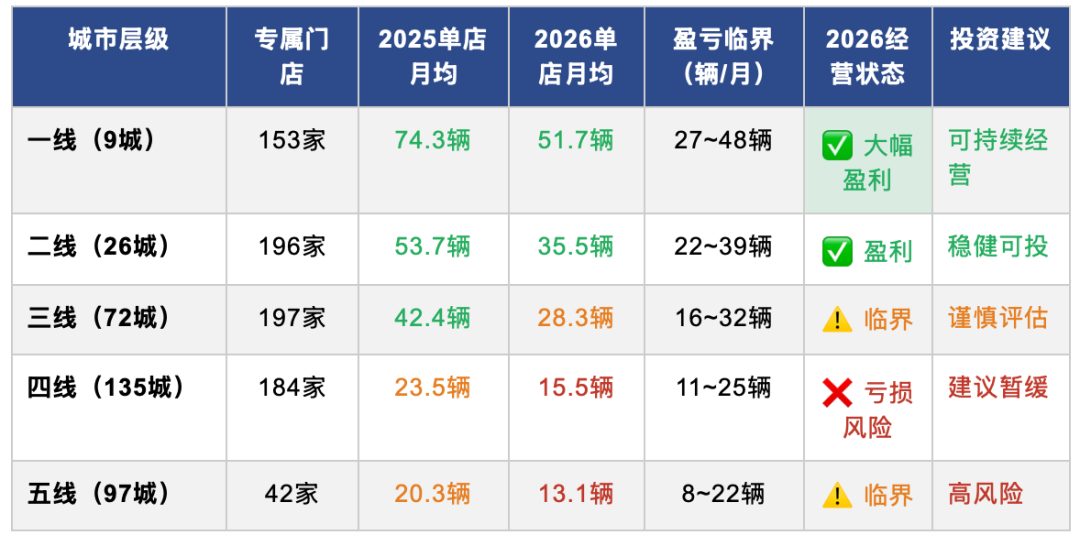

◆ 8.2 问界:渠道核心支柱,但热度已经退潮

问界是五界渠道体系中唯一能够独立支撑门店盈利的品牌。以下数据基于问界汽车专属门店(AITO用户中心),不含华为旗舰店等引流渠道,2025年为全年月均,2026年为1-4月月均。

数据口径:汽车专属门店(AITO用户中心),不含华为商超引流门店;盈亏临界含售后固定毛利(720台在保×1.5次/年×毛利率40%)

▸ 一二线城市仍是安全地带。一线单店月均51.7辆(临界27~48辆),二线35.5辆(临界22~39辆),均在盈利区间。BBA大幅折价导致的客群流失,持续向问界输送换购用户,是一二线门店保持健康的核心原因。

▸ 三线已到临界,四线实质亏损。三线城市单店月均28.3辆,处于盈亏临界区间底部;四线城市15.5辆,已明显低于临界值下沿(11~25辆)。从2025年到2026年,各层级单店月均普遍下滑约30%,市场热度较高峰期明显降温。

▸ 五线门店是高风险区域。42家五线问界专属门店单店月均13.1辆,处于盈亏边缘,门店数量少、销量体量薄,一旦品牌热度进一步下滑,将最先出现关停。

⚠️ 投资人需注意:问界2026年月均销量(23,223辆)较2025年全年均值(35,419辆)下滑约34%。单店数量仍在扩张,而销量在收缩——未来单店效能还可能进一步稀释。在四线及以下城市新开门店,需对这一趋势有充分预判。

◆ 8.3 鸿蒙智行共享门店(智界/享界/尚界):全线承压,依赖问界输血

智界、享界、尚界三界共享约1,287个汽车专属门店(物理去重),2026年合计月销约8,600辆,单店月均仅6.7辆——比问界四线城市(15.5辆)还低一倍以上,全面低于共享门店盈亏临界值(约5~16辆,视城市层级)。

三界月销无独立城市数据,按门店数比例估算;共享门店盈亏临界约5~16辆/月(单品牌分摊成本约为专属门店1/3~1/2)

▸ 一二线:单品牌视角深度亏损。一线共享门店盈亏临界约9~16辆,而三界合计单店月均仅6.7辆,按单品牌折算每个品牌不足3辆,高租金进一步放大亏损。

▸ 三四五线:临界生存,依赖问界补贴。三四五线运营成本相对较低,三界单店月均6.7辆勉强维持。但这些门店实际靠问界销量返利分摊维持整体收支——问界是"粮仓",三界是"搭车"。

▸ 三界处境各异,但均无法独立盈利。尚界从零起步增量明显(2025年9月上市);享界持续爬坡但折扣率达7.5%;智界折扣率高达10%,以价换量特征最突出。三界中无一能独立支撑共享门店盈利。

⚠️ 重要提示:共享门店获得智界/享界/尚界销售授权,不意味着增加实质性收入。当前三界每个品牌单店月销不足3辆,每增加一个品牌授权,展位资源和团队精力就需要进一步分散。对于现有问界经销商,增加三界授权可能不会提高收入,反而稀释问界的服务质量与客户体验。

◆ 8.4 尊界:精网逻辑自洽,适合特定经销商

尊界是五界中定位逻辑最为自洽的品牌:月销1,142辆,均价78.1万元,折扣率5.7%(五界最低,价格体系最健康)。以约313个专属汽车门店计算,全国单店月均约3.6辆,数字不高,但每辆车的单车毛利贡献(返利+金融+售后)约是问界的2~3倍。

▸ 一二线高度集中(97+121处=占比约69%)。高净值客群高度集中于高线城市,精网策略与目标客群地理分布高度吻合,不宜强行下沉。

▸ 适合有豪华品牌售后能力的经销商。尊界核心盈利来源是售后环节(保养、维修等),而非新车返利。这需要豪华车售后能力:高级技师、专用设备、VIP接待标准——具备BBA售后经验的经销商有天然优势。

▸ 四五线几乎无布局(仅9处),不宜强行入场。尊界购买逻辑与高线城市商务场景强绑定,三线以下城市目标客群稀少,得不偿失。

◆ 8.5 盈亏测算:问界A级门店参考模型(月销30辆)

收支项目 | 月度金额(估算) | 说明 |

▌ 收入端 |

|

|

新车交付返利 | 约20.7~25.9万元 | 满返4.3%~5.2%(含线索费等);让利后实际留存2%~2.5% |

金融保险收入 | 约8.3~9.3万元 | 单车毛利5,000元; |

售后服务 | 约10.8~15.1万元 | 720台在保×1.5次进厂/年;工单均值3,000~4,200元;毛利率40% |

月收入合计 | 约39.8~50.3万元 | 常态让利口径;满返口径可达63~78万 |

▌ 成本端 |

|

|

物业租金 | 约15~30万元 | 三线约10~15万,一线约27~33万,差距3倍 |

人员成本(约20人) | 约15万元 | 人均约7,500元/月 |

运营/水电/营销 | 约4~6万元 |

|

月成本合计 | 约28.4~56.8万元 | 三线28~35万;新一线41~49万;一线47~57万 |

月盈亏区间 | 三线+5~+22万;新一线−9~+9万;一线−17~+3万 | 地段选择是核心决策 |

注:以上为估算框架,实际受城市、地段、品牌运营能力影响较大;返利点位、金融参数来自行业参考,非官方数据,不构成投资建议

◆ 8.6 投资建议矩阵:六种情形,六种答案

投资人情形 | 建议评级 | 核心理由 |

一二线城市·现有问界门店·考虑扩网 | ★★★★ 积极考虑 | 单店月均35~52辆,盈利确定性高;在保车辆积累是售后长期基础;BBA客群仍在持续流入 |

一二线城市·有BBA豪华品牌经验·考虑代理尊界 | ★★★★ 值得评估 | 高客单价、低折扣(5.7%)、售后毛利丰厚;豪华品牌售后能力是核心门槛 |

三线城市·新建问界专属门店 | ★★★ 谨慎评估 | 单店月均28.3辆处于临界区间底部(16~32辆),盈利弹性小;须精细测算本地租金和客群,不建议盲目跟风 |

四线及以下城市·考虑新建任何品牌 | ★ 强烈暂缓 | 问界单店月均15.5辆已入亏损区间;三界月均不足7辆全面亏损;门店在扩张销量在收缩,时机不利 |

现有门店·考虑增加三界授权 | ★★ 冷静分析 | 三界单品牌月均不足3辆,无法独立盈利;增加授权更多是分散精力;等待某界出现爆款后再评估 |

任何城市·以"华为概念"为由仓促入场 | ⚠️ 需要警惕 | 品牌势能≠门店盈利;渠道扩张速度快于销量增速,竞争在加剧;四五线城市+三界品牌是当前最脆弱的组合 |

◆ 8.7 四项核心风险:投资前必须评估

▸ 风险① 华为战略依赖:所有渠道政策由华为主导,经销商自主空间有限。若华为战略调整(减少某界投入或调整分网政策),经销商无任何对冲手段。

▸ 风险② 各界分网竞争:智界/尚界独立建网后,同城将出现多家同品牌门店争夺同一客群,先入者地理优势被稀释;蛋糕不变但分蛋糕的人更多。

▸风险③ 均价持续下行:问界均价已从2024年的39.3万降至2026年的34.5万(两年降幅约12%);若M6等低价新品放量,单车返利收入将进一步压缩,门店盈利空间随之收窄。

▸ 风险④ 扩张期已过,效能分化期来临:2025年是渠道快速扩张期,门店数量与销量同步放大。2026年数据显示,销量下滑约34%而门店仍在增加——这意味着单店效能在被持续摊薄。现在是"精挑细选"而非"跑马圈地"的阶段:地段、品牌、层级的选择将决定未来3~5年的经营成败。

结语

鸿蒙智行的故事,本质上是中国科技品牌第一次系统性重构豪华车市场定价权的故事。它的成功不依赖补贴,不依赖价格战,而是依赖消费者可感知的技术体验优势和华为品牌的信任背书——这两者在当下的中国市场,比"百年工艺"更有说服力。

BBA的困境不是暂时的产品周期问题,而是智能电动时代竞争要素的根本性重构。折扣率从15%扩大到30%仍无法止住销量下滑,说明品牌溢价和产品力之间的缺口已超过价格手段所能弥合的范围。

未来三年,高端汽车市场最值得关注的是"BBA能否用技术反攻夺回话语权"。如果答案是否,中国品牌在高端市场的主导将从结构性机会变为结构性胜利。

数据说明:渠道数据来自网络公开信息;销量数据来自上险数据;盈亏测算基于行业参考数据估算,非官方数据。渠道数据、价量库数据、BBA折扣率、均价来自桑之未调研数据,并不代表车企真实数据,本报告内容仅供研究参考,本报告不构成任何投资建议,具体决策请结合实地调研、专业财务尽调及法律评估。

品牌研究|渠道的临界点 当出口撑起比亚迪的半壁销量,4700家国内门店怎么活?

数据|重车时代:新能源整备质量全景数据拆解

定价分析|产能利用率倒逼定价调整,上市十月个小米YU7推出23.35万入门款

数据分析|奥迪 E7X 预售28.98万起:上汽奥迪的"三层定价"试探

数据解析|500万辆库存压顶 4月车市正在经历一场无人公开谈论的危机

HIMA · Five-Realm System

Three Years of Huawei in Automotive: Disruption, Restructuring & Sustained Impact

Deep-Dive Research Report

Data period: Feb 2022 – Apr 2026 | Source: Vehicle Registration Data (VRD) / Public market information

May 2026 | For research reference only

Executive Summary

Metric | Value | Notes |

AITO Cumulative Sales | 1.07M | Feb 2022 – Apr 2026; market-validated milestone |

M9 Cumulative Deliveries | 285,000+ | 21 months; consecutive #1 in RMB 500k+ segment |

HIMA Monthly Sales (Apr 2026) | ~32,965 units | ≈ Lixiang (Li Auto); Five-Realm combined |

BBA 35k+ monthly sales decline | −85% (BMW peak) | Peak 160k → ~23k; pricing discipline collapsed |

The M9 achieved a milestone unprecedented in Chinese premium automotive history: 21 consecutive months as the unit-sales leader in the RMB 500k+ segment (Feb 2024 – Oct 2025), with an average market share of ~55% in the 500k+ NEV segment during that period, peaking above 70% in July 2024.

Chapter 1 Huawei's Strategic Logic in Automotive

◆ 1.1 Three Generations of Partnership Models

Huawei entered the automotive sector not as an OEM but as a technology enabler, progressively deepening its involvement as market evidence accumulated.

Model | Huawei Role | Key Partners | Core Characteristics |

Components Supply | Standardized module supplier | BYD Fang Chengbao, others | Supplies LiDAR, MDC; vehicle OEM retains brand control |

HI (Huawei Inside) | Full-stack intelligent solutions | Avatr (all), Voyah premium | Joint development; Huawei deep in ADAS & cockpit; OEM retains production/sales |

HIMA (Smart Selection) | Co-brand creator | Seres, Chery, BAIC, SAIC, JAC | Huawei co-defines product, design, marketing & sales; "X-Realm" brand; highest Huawei integration |

HI Plus / Yinwang (Three-Realm) | Full-stack co-creator (OEM retains final decision) | GAC (Qijing), Dongfeng (Yijing), SGMW (Huajing) | Deep R&D + equity ties; OEM brand independence; ADS 5 flagship / ADS Pro mass-market; covers RMB 150k–500k+ |

◆ 1.2 Huawei's Three Core Cards

The fundamental reason incumbents cannot replicate HIMA's success: Huawei simultaneously holds three assets unique in the automotive industry.

▸ HarmonyOS Cockpit: In-vehicle OS natively integrated with Huawei smartphones, smart home & enterprise ecosystem. The seamless experience moat cannot be reproduced by competitors in the near term.

▸ Qiankun ADS 4.0→5.0: End-to-end large-model architecture, city NOA expanding continuously, ADS 4.0 launched in 2025 — on par with XPENG and Tesla.

▸ Offline Distribution (Huawei Authorized Experience Stores): Thousands of Huawei retail locations become automotive sales touchpoints. Consumer profile for vehicle purchase and device purchase overlaps significantly; customer acquisition cost far below traditional 4S model.

Key Judgment: Huawei's advantage lies not in any single technology lead, but in the synergy of all three cards. Consumers buying AITO are fundamentally buying 'Huawei ecosystem membership' — a purchase-decision logic that BBA cannot counter with price cuts.

◆ 1.3 Three-Realm System: Strategic Extension of HI Plus (2025–2026)

The Five-Realm system's market success validated the value of 'Huawei endorsement' but also exposed the Smart Selection model's inherent tension — partner OEMs (Seres, Chery, BAIC, etc.) felt their autonomy was too constrained. The Three-Realm HI Plus model is Huawei's proactive response: offering major state-owned enterprises (Dongfeng, GAC, SGMW) greater decision-making autonomy while expanding Huawei's partnership footprint to cover all six major central/state automotive enterprises.

Brand | OEM Partner | Price Range | Launch | Technology |

Qijing | GAC Group | RMB 219,900–309,900 | Pre-sale May 29, 2026; delivery June | ADS 5 global first-fit + HarmonySpace 6 + 896-line dual-path LiDAR |

Yijing | Dongfeng | ~RMB 300k–520k (est.) | 2026 Q3 | ADS 5 global first-fit + 896-line LiDAR + CAS 5.0 six-axis collision avoidance standard |

Huajing | SGMW (Baojun) | RMB 149,800–193,800 | On sale May 8, 2026 | ADS Pro Enhanced + HarmonyOS Cockpit; ADS 5 Pro via future OTA |

◆ 1.4 ADS Technology Roadmap

Version | Launch | Core Capability | Representative Models |

ADS 3.0 | 2025 | Vehicle-to-parking 2.0; WEWA 1.0 architecture | M9/M8/M7; Zhijie R7; Xiangjie S9 |

ADS 4.0 | 2025 | Enhanced highway L3 | Zunjie S800; Shangjie H5/Z7 (factory-fitted) |

ADS 5 | Apr 2026 (first-fit) | WEWA 2.0; multi-agent gaming; L3 commercial deployment | Yijing X9 & Qijing GT7 (global first-fit); Five-Realm to catch up via OTA |

ADS Pro Enhanced | 2026 | Urban NCA accessible from RMB 150k | Huajing S (launch version) |

Chapter 2 HIMA Five-Realm System: From Breakthrough to Full Price Coverage

◆ 2.1 Five-Realm Brand Matrix

Brand | OEM | Launch | Apr 2026 Sales | Key Models | Strategic Position |

AITO (Wenjie) | Seres | Dec 2021 | 23,223 | M9/M8/M7 | Flagship; cumulative sales >1.07M; M7/M8/M9 span RMB 279,800–659,800 |

Zhijie | Chery | Dec 2023 | 2,385 | R7 | Sedan segment; R7 momentum fading; awaiting next product cycle |

Xiangjie | BAIC | Jun 2024 | 1,873 | S9 | Executive flagship sedan; targets government & corporate fleet |

Shangjie | SAIC | Sep 2025 | 4,342 | H5/Z7 | Most accessible; SUV+sports-crossover; H5 growing; Z7 launched Apr 22 (from RMB 219,800) |

Zunjie | JAC | May 2025 | 1,142 | S800 | Ultra-luxury flagship; S800 at ~RMB 789,800–1,028,000; low volume, high ASP |

Total | 5 OEMs | 4-yr span | 32,965 | 10 models | RMB 160k–1M+; full price-band penetration |

◆ 2.2 Sales Evolution: Three Phases

Phase | Period | Monthly Sales | Key Driver |

Single-model Breakthrough | Jan 2022 – Q2 2023 | 3,000–8,000 | M5 single-handedly validates Huawei channel conversion |

Hero Product Ignition | Q4 2023 – H2 2024 | 12,000–45,000 | New M7 re-launch (>20k/mo); M9 targets 500k+ crown; dual-engine established |

Full-Ecosystem Deployment | 2025–present | 53,000–93,526 | All Five Realms in production; M8 FY2025 champion (150k units); Dec peak 93,526 |

◆ 2.3 Brand-Level Status & Risks

AITO (Wenjie) — System Pillar; Monitor Model-Cycle Transition

▸ M9: 500k+ monthly sales eased from peak 18k (Jul 2024) to ~3,000–5,000 (early 2026); recovered to 7,500–9,200 in Q4 2025 post-2025MY launch. 21-month consecutive 500k+ unit-sales leader.

▸ M8: FY2025 champion — annual sales >150k, once had 90k order backlog; fills the RMB 350k–460k gap between M7 and M9.

▸ M7: FY2024 new-energy NEV annual champion; volume fluctuation during model refresh; M6 is ramping as successor.

Zhijie — Fading Momentum, Awaiting Product Refresh

▸ R7 monthly sales declined to ~1,910 units by April 2026; brand awareness significantly weaker than AITO.

▸ Discount rate rose from 6% to 9.5%, signalling competitive pressure. 'Zhijie 2.0 Strategy' announced with independent legal entity; new model launch expected to reactivate the brand.

Xiangjie — High Discount Rate and Volatile Sales

▸ S9 (executive flagship sedan) monthly sales 1,873 units; high volatility, unable to sustain consistent trajectory.

▸ BAIC deepening cooperation with Huawei; building Xiangjie-exclusive distribution network — lagging channel build-out is the primary constraint.

Shangjie — Rising Discounts; Z7 Upside Potential Unproven

▸ H5 stable at ~3,852 units/mo but discount rate accelerated: 4.89% (Oct 2025) → 11% (Apr 2026) — fastest discount deterioration across the Five Realms.

▸ Z7 launched Apr 2026 (490 units first month); as a sports-crossover, ramp trajectory needs more time to validate.

Zunjie — Ultra-Luxury Niche; Healthiest Pricing Discipline

▸ S800 priced at RMB 789,800–1,028,000; discount rate consistently 4.5–5.6% — the most disciplined pricing of all Five Realms.

▸ ~1,000 units/month; classic ultra-luxury small-volume product — Tier-1 cities contribute ~39% of sales, consistent with high-net-worth consumer profile.

Chapter 3 Distribution Network: Huawei's Third Core Card

Data source: HIMA official store locator (public information) | Snapshot: June 2, 2026 | Sales data: VRD, April 2026

◆ 3.1 Five-Realm Network Scale (June 2026 Snapshot)

As of June 2026, HIMA's Five-Realm system has approximately 5,960 authorized sales touchpoints (each brand counted independently). After deduplication by physical address, approximately 2,640 distinct outlet locations are identified, covering ~263 cities with ~90% national city coverage.

Brand | OEM | Auth. Touchpoints | Huawei Retail | Auto-Dedicated | Apr Sales | Strategic Position |

AITO | Seres | ~1,350 | ~570 (42%) | ~780 | 23,223 units | SUV flagship; M7/M8/M9 cover RMB 280k–660k |

Zhijie | Chery | ~1,410 | ~630 (45%) | ~780 | 2,385 units | Sedan segment; R7 fading; awaiting new product |

Xiangjie | BAIC | ~1,280 | ~570 (45%) | ~710 | 1,873 units | Executive flagship; network still expanding |

Zunjie | JAC | ~360 | ~44 (12%) | ~310 | 1,142 units | Ultra-luxury; selective network; few cities |

Shangjie | SAIC | ~1,560 | ~590 (38%) | ~960 | 4,342 units | Most accessible; H5 (from ~RMB 160k)/Z7 (~RMB 220k) |

Total | — | ~5,960 | ~650 (physical) | ~1,990 (physical) | ~32,965 | ~263 cities; ~90% city coverage |

Note: Authorized touchpoints include shared outlets (same physical outlet counted once per brand); physical outlets deduplicated by geographic location. All figures approximate.

◆ 3.2 Three-Tier Channel Structure

The HIMA distribution ecosystem comprises three distinct outlet types with clearly differentiated functions and brand coverage.

Channel Type | Physical Outlets | Primary Function | Brands Covered | Key Characteristics |

Huawei Flagship/Smart Life/Experience Stores | ~650 | Lead generation · Display · Order-taking (no delivery) | AITO + Zhijie only (other three not present) | Consumer electronics context; 2–3 display slots per store; store opex borne by Huawei |

HIMA User Centers (S/A/B tier) | ~1,320 (multi-brand shared) | Sales + Delivery + After-sales (integrated) | AITO/Zhijie/Xiangjie/Zunjie (by tier authorization) | ~93 S-tier flagships (≥8,000 m²) authorize all Five Realms; ~680 A-tier: four realms; ~370 B-tier: three realms |

Brand-Exclusive Networks (AITO Centers, etc.) | ~780 (AITO); others under construction | Brand-dedicated sales · Delivery · After-sales | Single brand only | AITO network most mature; Zhijie/Shangjie independent networks launched 2025; Shangjie: 1,500+ applications |

① Huawei Consumer Electronics Channel — AITO's Exclusive Traffic Funnel

Among ~650 Huawei flagship stores, Smart Life Halls, and authorized experience stores, AITO and Zhijie hold full display authorization across the network; Xiangjie and Zunjie have selective presence in premium flagship locations only; Shangjie has not yet entered Huawei retail channels (independent network under construction). The channel's value is not transaction volume but lead quality — consumers encounter automotive options naturally during device purchases, resulting in acquisition costs far below traditional 4S dealerships.

② HIMA User Centers — Brand Count Determined by Outlet Tier

Authorized Brands | Physical Outlets | Share | Outlet Type | Single-Brand Resource Share (est.) |

5 brands (all authorized) | ~93 | 3.5% | S-tier flagship User Center (≥8,000 m²) | ~20% |

4 brands | ~680 | 25.8% | A-tier User Center (3,000–8,000 m²) | ~25% |

3 brands | ~370 | 14.0% | B-tier User Center | ~33% |

2 brands | ~180 | 6.8% | City showroom / small User Center | ~50% |

Single-brand exclusive | ~1,320 | 50.0% | AITO-dedicated / brand-independent outlets | 100% |

③ Brand-Exclusive Networks — Fragmentation Accelerating

Brand | Independent Network Status | Scale | Key Milestones |

AITO | Mature | ~780 AITO-dedicated User Centers | Earliest to establish; operates in parallel with shared network |

Zhijie | Launched 2025; under construction | 100+ outlets (est.) | Independent legal entity; "Zhijie 2.0 Strategy"; Chery retains greater autonomy |

Xiangjie | Planning stage | ~21 physical exclusive outlets | BAIC building dedicated network; lagging channel is the primary constraint |

Zunjie | Selective network | ~5 independent outlets | Ultra-luxury positioning; selective strategy; not scale-driven |

Shangjie | Launched 2025; rapidly expanding | 1,500+ dealer applications | SAIC aggressively driving; applications already exceed existing official touchpoints |

◆ 3.3 Geographic Coverage: East & South Lead; ~49% in Tier-3 and Below

Province / Municipality | Physical Outlets (approx.) | AITO (approx.) | Commentary |

Guangdong | ~303 | ~167 | Largest network; GZ–SZ dual-core; full Pearl River Delta coverage |

Zhejiang | ~223 | ~126 | Driven by Hangzhou, Ningbo, Wenzhou, Taizhou; strong purchasing power |

Jiangsu | ~213 | ~121 | High density in southern Jiangsu (Wuxi, Suzhou) |

Shandong | ~158 | ~81 | Qingdao and Jinan lead; evenly distributed within province |

Henan | ~137 | ~57 | Zhengzhou ~48 outlets; strong Tier-3/4 city penetration |

Sichuan | ~126 | ~67 | Chengdu ~64 outlets; largest single-city western market |

Hunan | ~107 | ~39 | Changsha ~43 outlets; strong New Tier-1 consumer spending |

Fujian | ~103 | ~50 | Full coverage of Fuzhou–Xiamen–Quanzhou triangle |

Anhui | ~100 | ~39 | Hefei leads; rapid Tier-3/4 city penetration |

Shanghai | ~88 | ~47 | No.1 municipality; highest shopping-mall touchpoint density |

Beijing | ~77 | ~43 | Government & corporate client base; Zunjie has flagship presence |

City Tier | Physical Outlets | Share | Key Insight |

Tier-1 (Beijing, Shanghai, GZ, SZ) | ~277 | ~10% | Flagship concentration; highest shopping-mall display density; brand premium positioning |

New Tier-1 (~15 cities) | ~631 | ~24% | Strong Huawei brand loyalty; high NEV penetration rate |

Tier-2 (~20 cities) | ~430 | ~16% | High ADAS utilization; consumers receptive to technology premium |

Tier-3 and below | ~1,294 | ~49% | Deep penetration via Huawei CE channel; purchase conversion rate pending validation against sales data |

City unknown | ~8 | ~0% | Missing city field in API response |

◆ 3.4 Distribution Efficiency: Per-Outlet Productivity by Channel

Outlet efficiency analysis must distinguish between 'Huawei lead-generation touchpoints' (consumer electronics stores) and 'automotive-dedicated outlets' (User Centers, Experience Centers, Delivery Centers). The latter is the appropriate denominator for unit-sales efficiency.

Brand | Auto-Dedicated Outlets | Apr 2026 Sales | Monthly Units per Outlet | Assessment |

AITO | ~780 | 23,223 | ~30 units | Approaching BYD full-network average (~34); still on growth trajectory |

Zhijie | ~780 | 2,385 | ~3 units | Shared display space dominated by AITO; pre-new-product trough |

Xiangjie | ~710 | 1,873 | ~3 units | Network expansion outpacing product demand; S9 needs new product stimulus |

Zunjie | ~310 | 1,142 | ~4 units | Ultra-luxury selective network; absolute volume low; efficiency metric less relevant |

Shangjie | ~960 | 4,342 | ~5 units | Largest outlet count yet lowest efficiency; H5/Z7 ramp takes time |

* Monthly units per outlet = brand monthly sales ÷ automotive-dedicated outlet count. Huawei retail stores excluded from denominator.

Reference: BYD full-network ~34 units/outlet/month; BYD 4S dealership basis ~76 units/outlet/month (Jan–Apr 2026)

◆ 3.5 Structural Comparison with BYD's Distribution Model

Dimension | BYD | HIMA (AITO representative) |

Distribution model | Wide-area network: authorized dealers + city showrooms + sub-dealers (3-tier) | Selective network + traffic leverage: automotive outlets + Huawei CE retail |

Total physical outlets | ~3,400 (all dedicated automotive) | ~2,640 (incl. ~650 Huawei CE outlets) |

Monthly units per outlet | ~34 (full network); ~76 (4S dealership) | AITO: ~30 (auto-dedicated basis); ~17 (all touchpoints) |

Tier-3 and below coverage | ~2,400 outlets; below breakeven threshold | ~49% (~1,294 outlets); conversion efficiency pending validation |

Channel cost | High capex per outlet; city showroom closures accelerating (net −600 in Q1) | Huawei retail opex borne by Huawei; automotive display = marginal cost increment |

Core advantage | Scale coverage; full price band; unmatched Tier-3/4 penetration | Huawei ecosystem traffic; shared outlets reduce per-brand buildout cost |

Core risk | Tier-3/4 efficiency under pressure; showroom closures hurt dealer confidence | Zero-sum display competition in shared centers; brand fragmentation weakens collective network |

◆ 3.6 Network Fragmentation Tension: Independent Networks vs. Collective Synergy

Of ~1,320 multi-brand shared outlets, ~93 hold full Five-Realm authorization, ~680 hold four-brand authorization, and ~370 hold three-brand authorization. The more brands authorized, the thinner the display resources available to any single brand — this is the quantitative expression of the network's internal tension.

▸ Zhijie and Shangjie have announced independent distribution networks; Xiangjie is planning one. AITO established its ~780 dedicated User Centers long ago.

▸ Independent networks enable brand-specific buildout standards, reducing dealer pressure — but dilute the collective synergy effect of the HIMA umbrella brand.

▸ AITO's ~780 dedicated User Centers have the strongest brand independence; the remaining Four Realms remain highly dependent on the shared network.

Data note: Channel figures sourced from HIMA official store locator (public data, June 2026 snapshot). All figures approximate. Sales data: VRD, April 2026. For research reference only.

Chapter 4 Product Competitiveness: Why AITO Holds the RMB 400k+ Market

◆ 4.1 Competitive Configuration Benchmarking

Configuration data sourced from automotive specifications database; subject to change. Please verify against official OEM specifications.

Model | Price (RMB 10k) | Powertrain | Charging | Battery | Key Differentiation |

AITO M9 | 47.98–65.98 (2026MY incl. LWB) | EREV / BEV | EREV 400V / BEV 800V | CATL | HarmonyOS Cockpit + full-stack Huawei ADAS + CAS 5.0 six-axis collision avoidance (standard across all trims) |

AITO M8 | 35.98–45.98 | EREV / BEV | EREV 400V / BEV 800V | CATL | M9 tech trickle-down; best value in lineup |

AITO M7 | 27.98–37.98 | EREV / BEV | EREV 400V / BEV 800V | CATL | FY2024 new-energy NEV annual champion |

Lixiang L9 | 45.98–50.98 | EREV | 400V | CATL (52 kWh) | 6-seat large SUV; family-first positioning; extended range (no high-voltage DC) |

NIO ES8 | from 49.60 | BEV | 900V | CATL (102 kWh) | Battery swap model; ultra-high-voltage fast charge |

YangWang U8 | 100.80 | EREV | 800V hi-voltage | Fudi (56.58 kWh) | Off-road flagship; ultra-luxury positioning |

◆ 4.2 Four Pillars of AITO's Product Competitiveness

① EREV Powertrain: Precisely Aligned with Chinese Consumer Needs

▸ M9 EREV variant captures ~85–92% of sales volume (ASP ~RMB 480k); BEV only 8–15% — users are actively choosing EREV, not accepting it as a fallback.

▸ EREV resolves the core pain point for premium Chinese consumers: zero range anxiety on long trips; EV mode for daily commuting; no charging-convenience tradeoff.

▸ Transaction discount rate of only 5–7%, vs. same-segment BBA at 20–30%. Residual value ranked #1 among large SUVs for 9 consecutive months.

② Huawei Full-Stack ADAS (ADS 3.0): A Generational Experience Gap

▸ End-to-end large-model architecture; map-free city NOA with continuous OTA improvement; real-world experience leads most competitors.

▸ AITO M9 NPS of 85.2 in 2025, consistently #1 in overall model rankings — intelligent driving is the top recommendation driver among owners.

▸ BBA ADAS systems lag ADS 3.0 by a meaningful generation; BBA's delayed EV transition prevents rapid catch-up.

③ HarmonyOS Cockpit: Ecosystem Stickiness Creates an Unassailable Moat

▸ Hundreds of millions of Huawei smartphone users are pre-qualified potential buyers — the vehicle-device connectivity experience creates strong lock-in.

▸ HarmonyOS in-vehicle supports multi-screen linkage, remote vehicle control, and wearable device integration — impossible for competitors to replicate this ecosystem synergy.

④ Huawei Retail Distribution: Low-Cost Acquisition, Premium Brand Endorsement

▸ Huawei Authorized Experience Stores serve as vehicle display and first-contact points; purchase decisions arise naturally from digital consumer contexts.

▸ Huawei's technology premium in consumer mindshare transfers directly to AITO vehicles; owners willingly pay RMB 400k–500k for 'a Huawei car'.

Chapter 5 Competitive Landscape: Diminishing Returns of Huawei Enablement & the Three-Realm Dilemma

The data points to a core structural issue: the success or failure of HIMA's Five-Realm system ultimately depends on how much differentiated value Huawei's technology and brand can deliver at each price point. The evidence shows this value decays rapidly as prices decline — above RMB 350k, 'a Huawei car' is a genuine premium justification; below RMB 200k, the label has limited incremental appeal.

(See competitive landscape positioning chart — inserted in full report)

Fig.: Five-Realm Competitive Landscape | Circle size = competitor monthly sales | Coloured circles = Five-Realm brands | Data: Apr 2026 VRD

◆ 5.1 AITO & Zunjie: Strategy Sound, Moat Genuine

AITO's core competitive thesis is capturing customers during BBA's delayed intelligent transformation. From 2024 to 2026, combined BBA monthly sales were halved — from ~165,000 units to ~96,000 — while transaction discounts broke through 20%+ across the board (Audi 27.5%, BMW 23.3%, Mercedes 19.5%), signalling a collapse in pricing discipline, with massive client migration flowing to AITO.

However, this window is not permanent. BBA's lag in intelligent driving is a timing gap, not a capability gap — Mercedes and BMW have both entered deep partnerships with Chinese ADAS suppliers, with L2+ capable models expected by 2026–2027. AITO's current advantage is fundamentally an interception dividend during BBA's transition. The window is estimated at 2–3 more years — which is precisely why AITO is aggressively expanding its distribution network and mindshare during this period.

Zunjie's positioning is internally consistent. Monthly sales of 1,142 units, ASP of RMB 781k, discount rate 5.7% — an ultra-luxury brand not optimizing for volume but for establishing Huawei's brand anchor in the RMB 1M+ market. The logic mirrors AITO: capturing the pricing vacuum left by aggressively discounting BBA luxury models with technology premium.

◆ 5.2 The Three-Realm Dilemma: Wrong Battlefields or Overambitious Strategy?

Zhijie, Xiangjie, and Shangjie have entered price segments with numerous competitors each possessing comparative advantages — and Huawei's technology enablement cannot serve as a decisive purchase trigger in these segments. Launching more models solves 'whether there's anything to buy,' but not 'why should I buy yours.'

① Zhijie: Stuck in a fiercely competitive SUV segment with insufficient differentiated competitiveness

n April 2026, monthly sales of the Zhijie R7 (a mid-to-large SUV) stood at 1,910 units. By comparison, Li Auto i6 recorded monthly sales of 21,003 units (over 11 times higher), Xiaomi YU7 hit 9,828 units (5 times higher), and AITO M7 achieved 8,628 units (4.5 times higher). Boasting solid reputation for extended-range powertrains and family-focused positioning, Li Auto i6 takes an upper hand; meanwhile, Xiaomi YU7 gains edge thanks to a modest 2.0% discount rate and strong brand influence, collectively building formidable advantages in the 200,000–300,000 RMB mid-to-large SUV market.

Source: Vehicle Sales & Pricing Database, April 2026 VRD

Its 8.8% discount rate speaks volumes: while rival SUVs in the same segment keep discount levels between 2% and 6%, Zhijie has to slash prices to prop up shipments, an indication the product fails to command a pricing premium against competitors. Chery boasts mature vehicle engineering capabilities, yet its brand strength falls short of justifying the pricing premium corresponding to Huawei’s integrated technologies. Instead of rolling out more new models, Zhijie needs a blockbuster SUV capable of cultivating an irreplaceable market reputation within the segment.

② Xiangjie: Most Awkward Positioning — Purchase Logic Awaits Structural Shift

Xiangjie S9 at RMB 320k–400k targets the executive sedan market — caught between heavily discounted BBA models above (Mercedes C-Class still carries brand equity) and high-value NEV upstarts below (Xiaomi SU7 Pro at RMB 285k). More fundamentally, the core purchase driver for executive sedans is 'social signaling in business contexts' — a logic not yet restructured in the NEV era. Buyers may still prefer a discounted Mercedes over Xiangjie S9 for corporate client entertainment. This is a timing and perception issue, not a product quality issue; more models cannot accelerate the shift.

③ Shangjie: Entering a Battlefield Where the Huawei Brand Barely Helps

In the RMB 150k–200k segment, consumer purchase priorities are reliability, residual value, and cost-effectiveness — not ADAS experience or HarmonyOS cockpit smoothness. The customer profile in this segment differs materially from AITO's core buyers (high-income consumers seeking premium intelligent experience), and Huawei's brand premium is nearly impossible to monetize here. SAIC has a powerful distribution mobilization capacity (1,500+ dealer applications), but using distribution scale to compensate for product differentiation deficiency will only accelerate attrition.

◆ 5.3 A Concise Structural Conclusion

Brand | Segment | Huawei Enablement Effectiveness | Strategic Assessment |

AITO | Premium SUV (RMB 300k–550k) | High — exactly the BBA trade-up target segment | ✅ Clear logic; well-executed |

Zunjie | Ultra-luxury (RMB 800k+) | High — ultra-luxury buyers prize technology premium | ✅ Selective network; low volume, high quality |

Zhijie | RMB 200k–300k sedan | Medium-low — segment is not short of smart-tech brands | ⚠️ Segment selection questionable |

Xiangjie | Executive sedan (RMB 320k–400k) | Medium — B2B purchase logic not yet restructured | ⚠️ Passively waiting for consumer mindset shift |

Shangjie | RMB 150k–200k SUV | Low — purchase logic misaligned with Huawei enablement | ❌ Wrong battlefield |

The Five-Realm system is fundamentally a 'two-strong, three-weak' structure rather than a balanced five-brand portfolio. AITO and Zunjie's success is supported by clear competitive logic; Zhijie, Xiangjie, and Shangjie face not execution problems but segment-selection problems — in their respective price bands, Huawei's differentiated value is not yet sufficient to be the dominant purchase driver. More new models from these three, absent systemic change in their competitive environments, will not meaningfully change the volume trajectory.

Chapter 6 Impact on Premium Brands: Data Confirms Substitution Effect Is Real

◆ 6.1 Power Shift in the RMB 400k+ Market

In February 2024, AITO first appeared in the RMB 400k+ segment with an ASP of ~RMB 509k. Two months later, AITO ranked third in that market (behind only Mercedes and BMW), with monthly sales exceeding 13,000 units — while Audi in that segment had already fallen to 3,000–5,000 units.

Brand | Discount Rate Early 2023 | Discount Rate 2026 | Deterioration | RMB 350k+ Sales Change |

BMW | 14.4% | 23.5–28.8% | +14pp | −91.1% |

Mercedes-Benz | 7.9% | 19.3–21.7% | +12pp | −80% |

Audi | 18.1% | 27.2–29.0% | +11pp | −96.2% |

Porsche | 3.8% | 11.3–15.7% | +10pp | Gradual decline |

Lexus | 7.4% | 17.6–19.7% | +14pp | Gradual decline |

◆ 6.2 Three Dimensions of Substitution

① Direct Volume Substitution

▸ Chinese premium brands' share of the RMB 300k+ market surpassed 35% in H1 2025, up from less than 10% five years ago; in the RMB 500k+ segment, share exceeded 60%.

▸ Some BBA dealers have begun transitioning to Chinese NEV brands; distribution resources are migrating.

② Consumer Mindshare Substitution

▸ A significant share of AITO M9 owners traded in BBA vehicles. High-net-worth consumers are adopting M9 as 'the new luxury identity statement.'

▸ M9 ranked #1 in residual value among large SUVs for 9 consecutive months — shattering the 'Chinese cars have poor residual values' stereotype. This is the hardest barrier to overcome in brand ascent.

▸ Consecutive NPS #1 rankings indicate powerful owner advocacy, creating an organic word-of-mouth flywheel.

③ Technology Premium Restructuring

▸ Traditional premium brand pricing power derived from engine tuning, chassis engineering, and brand heritage — attributes whose weighting in the intelligent-EV era is declining.

▸ Huawei ADS ADAS, HarmonyOS Cockpit, and continuous OTA evolution represent the new 'technology premium' — one that consumers experience daily, not just when deciding to purchase.

▸ BBA's NEV offerings (BMW iX, Mercedes EQS, etc.) are also suffering significant discount expansion, confirming that brand premium does not transfer effectively to electric platforms.

Chapter 7 Will the Disruption Persist? Structural Assessment

◆ 7.1 Three Structural Forces Supporting Continued Disruption

Force 1: Technology Moat Continues to Deepen. Huawei ADS undergoes quarterly OTA iterations. BBA is choosing partnerships with Momenta rather than in-house development — BMW's New-Generation iX3 adopts Momenta's solution (target 2026 year-end launch); SAIC Audi E7X launched at Guangdong–HK–Macao GBA Auto Show May 29 (from RMB 269,800), first-fitting Momenta R7. However, Momenta + joint-venture combinations can only compete with Huawei Qiankun on the single ADAS dimension; they cannot replicate Huawei's full-stack 'vehicle–device–home' ecosystem advantage.

Force 2: Pricing Discipline Relatively Intact, Discounts Not Yet Out of Control. AITO M9 discount rate holds at 5–7%, preserving ample brand premium vs. BBA's 20–30%. Shangjie's rising discount (11%) warrants monitoring, but the flagship M9's healthy discount serves as a system stabilizer.

Force 3: Product Matrix Expanding, Price Bands Continuously Penetrating Downward. Shangjie H5 (from RMB 159,800) marks HIMA's first entry into the sub-RMB 200k market. The Five-Realm system now spans approximately RMB 160k to RMB 1M+, materially expanding addressable consumer reach.

◆ 7.2 Three Risks to Monitor

Risk 1: Inter-Brand Cannibalization — Distribution Resource Competition

Ten Five-Realm models concentrated in Huawei stores and HIMA User Centers has exceeded single-outlet carrying capacity, intensifying display-slot competition. Zhijie and Xiangjie have initiated independent network builds ('X-Realm 2.0 Strategy') — a necessary growth step, but also signals declining direct Huawei control, adding pressure to brand differentiation.

Risk 2: Partner OEM Bargaining Power Dynamics

As the Smart Selection model matures, partner OEMs (Seres, Chery, etc.) face growing technology and brand dependence on Huawei. Should the partnership structure change, each brand's standalone operational capability is uncertain. Simultaneously, the long-term risk of partner OEMs having their own technology accumulation marginalized persists.

Risk 3: BBA Counter-Offensive — Not Inconceivable

▸ BMW New-Generation iX3 equipped with Momenta ADAS (target launch end-2026); ASP ~RMB 300k–400k, directly targeting AITO M7/M8 segment. SAIC Audi E7X launched at GBA Auto Show May 29 (RMB 269,800–359,800), positioned between Lixiang i8 and NIO ES6 with aggressive pricing.

▸ Mercedes MB.OS architecture advancing EV transformation; joint-venture brands accelerating localization with domestic ADAS providers. Audi E7X's 'German driving dynamics + Chinese ADAS' combination is a new template for joint-venture brand counterattack.

▸ BBA still maintains tens of thousands of annual sales units in China; brand heritage, engineering foundation, and global reach retain effectiveness with a subset of consumers.

Risk 4: Momenta + Joint-Venture Alliance — Most Substantive ADAS Challenge

BBA has chosen deep partnership with Momenta rather than self-development. Momenta has become the dominant third-party ADAS supplier domestically, and is penetrating the RMB 300k+ premium market across multiple joint-venture brands — the most direct competitor to Huawei Qiankun in intelligent driving.

Dimension | Momenta + Joint-Venture | Huawei Qiankun (HIMA) |

ADAS capability | WEWA architecture; R7 reinforcement learning world model; same tech generation as ADS 5 | WEWA 2.0; multi-agent gaming; ADS 5 with 10× training uplift vs. prior generation |

Ecosystem | Pure ADAS algorithm supplier; no cockpit OS, cloud, or connected-device integration | Full-stack: ADAS + HarmonyOS Cockpit + vehicle cloud + in-car optics + wearable linkage |

Brand endorsement | None — Momenta brand invisible to consumers; OEM brand carries | Huawei brand directly visible; "Huawei inside" is a purchase trigger |

Scale | 20+ brands, 60+ models at Beijing Auto Show; 70M+ units delivered (city NOA) | Concentrated on 5+3 brands; deeper integration per brand; unified OTA cadence |

Verdict | Effective competition on ADAS dimension alone; cannot replicate full-stack ecosystem | Full-stack integration advantage sustained; ecosystem premium strongest in 300k+ segment |

◆ 7.3 Synthesis: Disruption Persists, but Enters Deeper Competitive Waters

Near-term (2026–2027): HIMA's dominance in the RMB 400k+ market is largely established; M9 retaining 500k+ leadership is highly probable; BBA counter-offensive impact is limited.

Medium-term (2027–2029): As BBA next-generation products launch, the premium segment will enter a more intensive technology competition phase. Huawei must sustain generational leadership in ADS and HarmonyOS Cockpit. AITO M9's residual value advantage sustaining will be the key validation metric for pricing power.

Long-term (2029+): Outcome depends on Huawei intelligent driving ecosystem's global expansion capability, and whether Chinese premium brands can replicate domestic success in overseas markets. If AITO's international pathway is established, the disruption of traditional premium brands extends from China to global markets.

Chapter 8 Dealer Investment Decisions: The Real Picture Behind the Numbers

The distribution analysis ultimately surfaces a practical question: as an automotive dealer investor, should you still be investing in HIMA outlets? The following provides a structural framework — not generic advice — based on the data in this report.

◆ 8.1 Industry Context: NEV Dealer Polarization Intensifying

In 2025, approximately 55.7% of China's automotive dealers reported losses — traditional ICE 4S dealerships bearing the brunt. By contrast, NEV-brand dealers reported profitability at ~43%, significantly outperforming the industry average (23.5%). However, 'NEV dealer' is itself a bifurcated category — profitability concentrates in premium brands, high-ASP models, and top-tier outlets; tail outlets face challenges indistinguishable from ICE 4S difficulties.

◆ 8.2 The Most Critical Numbers: Five-Realm Per-Outlet Efficiency Divergence

Brand | Auto-Dedicated Outlets/Month | 4S-Basis Monthly Units | Discount Rate | Investment Risk | Key Variable |

AITO | ~30 units (auto-dedicated) | 58.9 units (4S basis) | 5.0% | ★★☆ Medium-Low | M8/M9 volume sustainability; Huawei strategic continuity |

Zhijie | ~3 units | 6.4 units | 10.0% | ★★★★ High | Must await Zhijie 2.0 new models; currently deeply loss-making |

Xiangjie | ~3 units | 5.6 units | 7.5% | ★★★★ High | BAIC network lagging; S9 product iteration is key |

Zunjie | ~4 units | — (not tracked) | 5.7% | ★★★ Medium | Ultra-luxury selective; low volume but high ASP; aftersales margin rich |

Shangjie | ~5 units | — (not tracked) | 8.3% | ★★★★ High | H5/Z7 ramping; 1,500+ network applications but intensifying competition |

Data: Unit estimates sourced from (1) public data; (2) Vehicle Sales & Pricing Database (research data; differences from OEM-reported data exist; for reference only). 4S-basis monthly units = brand monthly sales ÷ database 4S outlet count.

AITO's 4S-basis monthly throughput of 58.9 units indicates a meaningful share of existing AITO dealers are profitable — underpinned by 20,000+ monthly unit sales scale and the inventory-free order model (dealers carry zero stock; vehicles arrive for immediate delivery). Zhijie/Xiangjie per-outlet monthly throughput below 7 units is well below most estimated breakeven thresholds (~20–30 units/month), with current operators largely surviving on after-sales service revenue accumulation.

◆ 8.3 Investment Guidance: Three Investor Profiles, Three Answers

Investor Profile | Recommendation | Rationale |

Existing BBA luxury brand experience Tier-3 or below city location Capital available (RMB 5M+) | Actively consider AITO network | Customer profile overlap is high; rent is manageable, breakeven achievable; AITO 4S-basis monthly throughput of 59 units far exceeds breakeven |

Tier-1/2 city new entrant No luxury brand experience Seeking Zhijie / Xiangjie / Shangjie | Defer; wait for timing | High rent burden; Three-Realm per-outlet monthly throughput <7 units; standalone operation persistently loss-making; wait for respective new product launches before re-evaluating |

Existing AITO authorization Considering expansion or adding brands | Consider expanding AITO network | In-warranty vehicle base is the foundation of after-sales profitability; single-brand depth outperforms multi-brand dilution; adding Zunjie authorization (if S-tier qualified) merits evaluation |

Core Risk Disclosure: ① Huawei Strategic Dependency — all channel policies controlled by Huawei; dealer autonomy is limited. ② Network Fragmentation Competition — same-brand stores in the same city will dilute first-mover advantages. ③ ASP Pressure — AITO ASP has declined from RMB 393k (2024) to RMB 345k (2026); per-unit rebate income is compressing. ④ Investment Payback — typically 3–5+ years; adequate capital reserves and risk tolerance are prerequisites.

Conclusion

The HIMA story is fundamentally the first systematic repricing of luxury automotive by a Chinese technology brand. Its success relies not on subsidies or price wars, but on verifiable technology experience advantages and the trust equity of the Huawei brand — two factors that, in today's Chinese market, are more persuasive than '100 years of craftsmanship.'

BBA's predicament is not a temporary product-cycle issue. It is a fundamental restructuring of the competitive attributes that matter in the intelligent-EV era. Transaction discounts expanding from 15% to 30% while volume still declines confirms that the gap between brand premium and product capability has exceeded what pricing instruments can bridge.

The pivotal question for the premium auto market over the next three years: Can BBA mount a technology counter-offensive to reclaim market primacy? If the answer is no, Chinese brands' dominance in the premium segment will evolve from a structural opportunity into a structural victory.

Data Disclosure: Sales data in this report sourced from Vehicle Registration Data (VRD). Channel data, pricing database data, BBA discount rates, and ASPs are research-compiled data; they do not represent OEM-reported figures and are for reference only. This report does not constitute investment advice.